SCHD Q2 Dividend Announced: How Much You’ll Get Paid

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

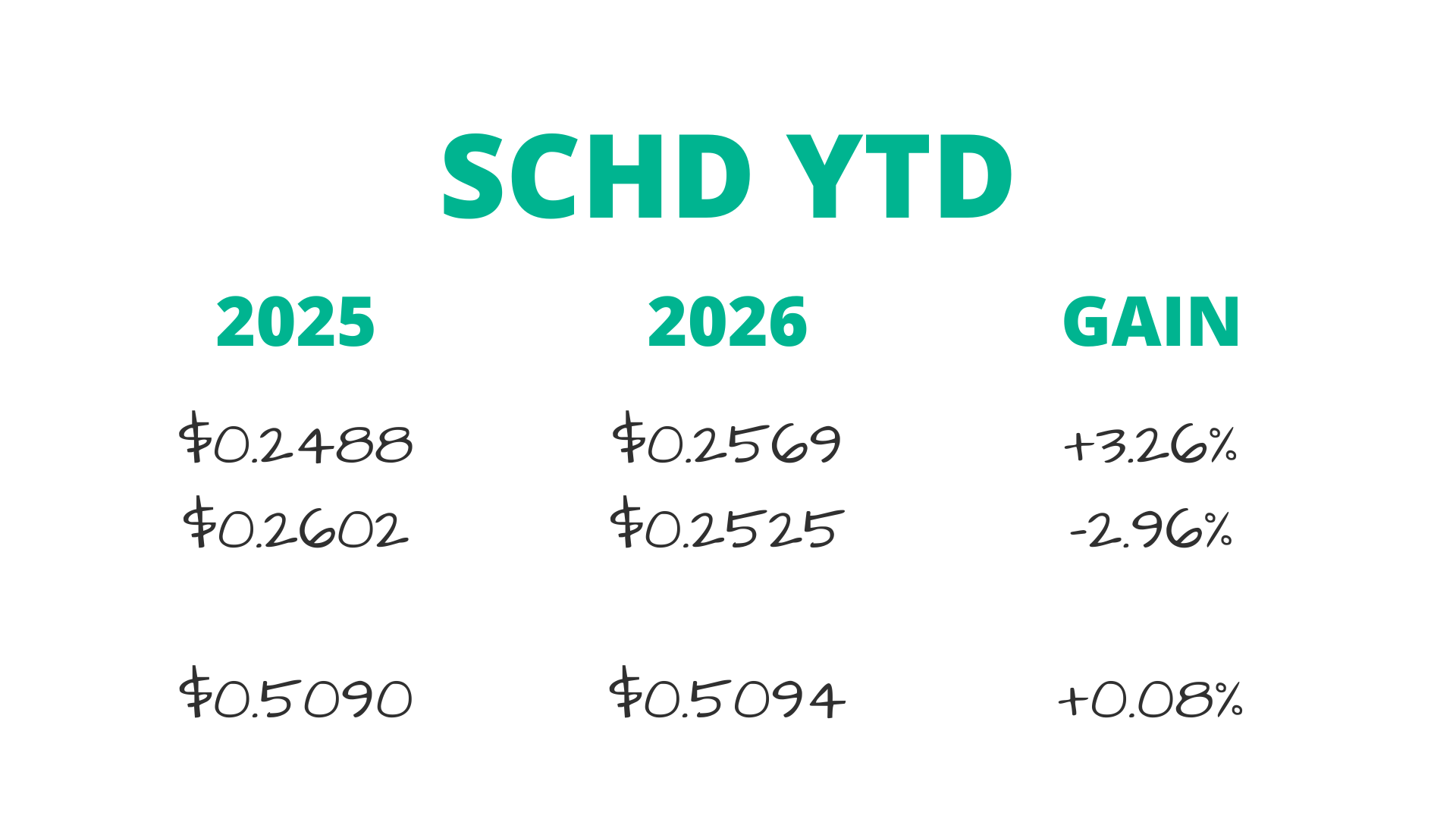

By now, there's a good chance you've already heard that SCHD just announced its upcoming dividend payment for Q2, coming in at $0.2525 per share to be paid on June 29th.

Admittedly, I was expecting a slightly higher payment for this quarter, and it seems I wasn’t the only one. Many of the estimates I saw were predicting at least $0.26 per share, and I don’t think anyone was expecting this quarter's payment to come in lower than last year's.

For reference, SCHD paid $0.2602 per share in Q2 2025, meaning this quarter's payment represents about a 3% decrease year-over-year.

With that said, if we combine the first two payments of 2026, that'll bring the total dividends per share so far this year to $0.5094, which is pretty flat compared to the first two quarters of last year, where the fund paid out $0.509.

From what I've seen in the comments on my recent video announcing the news, and from what I've read on Blossom, SCHD’s dividend performance so far this year is causing some investors to jump ship and sell out of the fund.

Personally speaking, I understand the frustration since this type of dividend performance is so uncharacteristic of the fund. Still, it's important to remember that what happens in one quarter, or two quarters, or even three or four quarters doesn't mean all that much in the grand scheme of things.

One disappointing quarterly payment, in my opinion, shouldn’t be enough for long-term investors to throw in the towel, especially when there are still two distributions left to be paid this year.

Plus, SCHD's share price returns have been on fire here in 2026. Shareholders have still done pretty well from a total-return perspective.

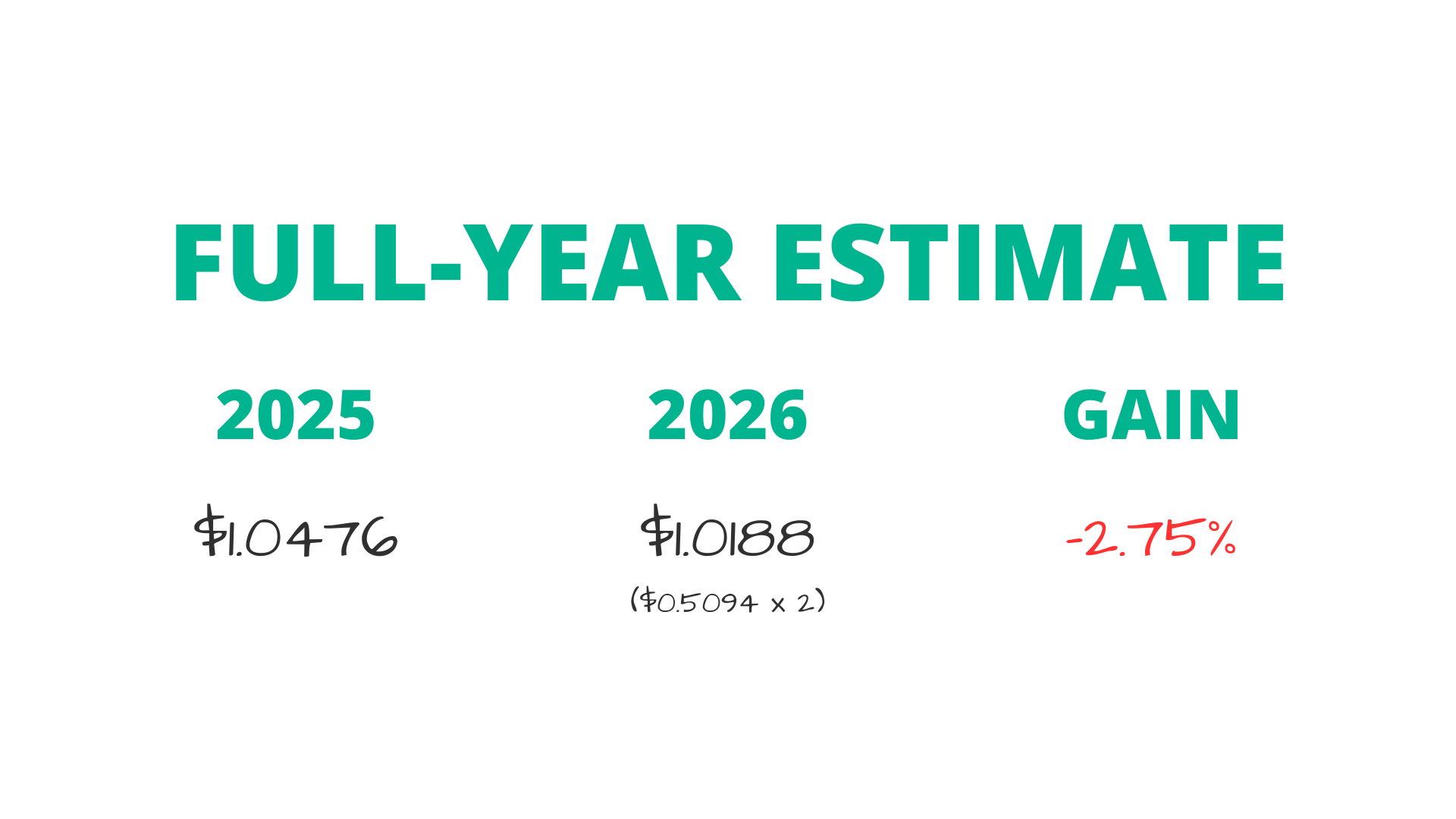

With that said, I think it's reasonable to hope that SCHD's payments in the back half of the year follow last year's trends, where we saw higher payments in Q3 and Q4 than we did in Q1 and Q2.

We definitely need that to happen, actually, or else we might be seeing SCHD's first-ever reduction in annual dividends.

In fact, if SCHD were to simply repeat its first-half payments in the back half of the year, the fund would end 2026 paying out slightly less in annual dividends than it did in 2025.

I'd be very surprised if that ended up being the case. But still, it's a crazy world, and anything's possible.

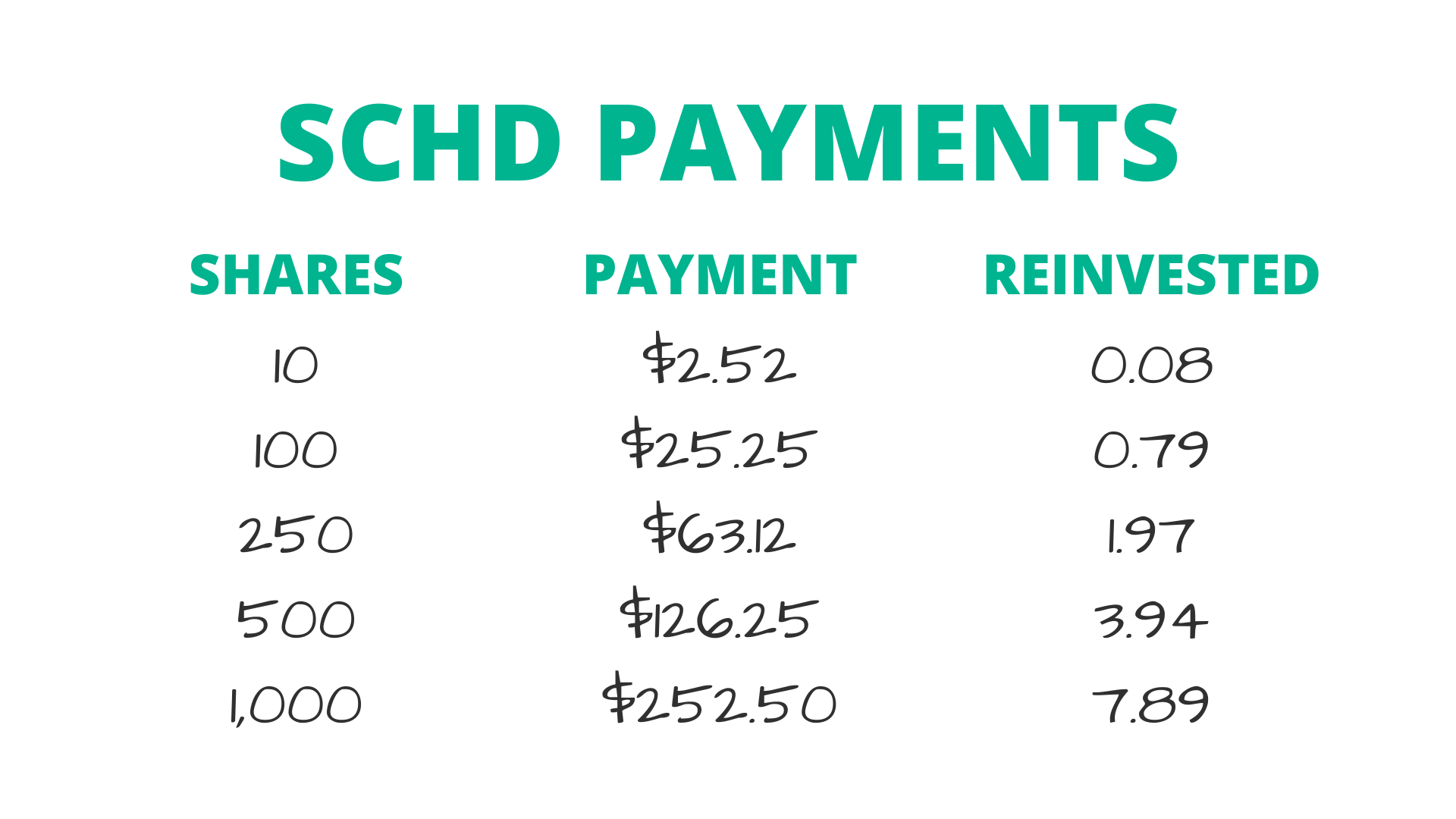

Nonetheless, with this quarter's payment officially announced, let's break down what that means for shareholders. The graphic below shows what you can expect to be paid, and how many shares you will get when reinvested, based on different share counts.

Personally speaking, I have 571 shares of SCHD in my Roth IRA on Public. And since SCHD will be paying out $0.2525 this quarter, with the 571 shares in my portfolio, I should be getting a paycheck for just over $144.

Reinvesting that dividend payment back into the portfolio should get me an extra 4.5 shares, which will take my position from 571 shares up to about 575.5 shares. And that's exactly why I love dividend investing, and refer to it as “the gift that keeps on giving.”

Every dividend payment buys more shares, and those extra shares go on to generate even more dividends the next time around. As long as those dividends continue to get reinvested, that snowball just keeps getting bigger and better over time.

Having said that, now I'd love to hear from you: What do you think of this quarter's payment, and how many shares of SCHD do you have in your portfolio? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

IN MY PORTFOLIO 📈

See my full portfolio with all of my holdings, trades, and dividends on Snowball Analytics! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

Reacting To Subscriber Portfolios

In this video, I'm reviewing three subscriber portfolios, one of which is a $380,000 dividend portfolio paying over $1,000 every single month.

CAREFULLY CURATED 🔍

📺 The Dividend Advantage - According to Gen Ex Dividend Investor, the biggest benefit of dividend investing may have nothing to do with the actual income.

🎧 Shameless Cloner - On this recent episode of the My First Million podcast, Mohnish Pabrai explains how borrowing ideas from multiple disciplines can substantially improve your decision-making, especially in the realm of investing.

📚 The Great Squeeze - This is part one of a three-part essay series from James Emanuel discussing why so many people feel like they're falling behind despite doing all the "right" things.

SINCE YOU ASKED 💬

"Can you explain assets under management (AUM) and yield on cost (YOC)? I noticed that VT has a lower AUM than VTI, even though VT holds more companies. Also, I've tried to understand YOC, but it never seems to click for me."

- Ethan | YouTube

I can definitely explain these for you. Great questions!

Starting with assets under management (AUM), this term basically just describes the total amount of money invested in a particular fund. It doesn't have anything to do with how many different companies the fund holds.

For example, even though VT holds more companies than VTI (over 10,000 compared to about 3,500), VTI has many more dollars invested in it. As I'm writing this, VTI has about $660 billion in assets under management, while VT has about $76 billion.

Now getting into yield on cost (YOC), this is a concept that confuses a lot of investors when they first come across it. You're definitely not alone there.

You're probably already familiar with the dividend yield, which measures the annual dividend paid per share relative to the stock's current share price. Yield on cost is similar, except it measures the annual dividend paid per share relative to the price you originally paid for the stock. That's the only difference.

Let's use Coca-Cola (KO) as an example. As I'm writing this, KO pays an annual dividend of $2.12 per share and trades for $79.39 per share. That gives the stock a current dividend yield of 2.67%.

Hypothetically, if you bought KO today at $79.39, your yield on cost would also be 2.67%.

Now let's say KO goes up to $90 per share while continuing to pay that same $2.12 annual dividend. The stock's current dividend yield would go down to 2.35% because the dividend per share is now being divided by a higher share price.

However, your yield on cost would still be 2.67% because your original purchase price is still $79.39. That didn't change.

The reason many dividend investors track yield on cost is because it shows how much income you're generating relative to the amount you originally invested. Over time, if a company continues raising its dividend, your yield on cost can grow pretty substantially even if the stock's current yield doesn't change all that much.

Expanding on our KO example, let's say the company continues its 60+ year dividend growth streak and eventually raises its annual dividend from $2.12 per share to $2.50 per share. At your same $79.39 cost basis, your yield on cost would go from 2.67% up to 3.15%. And if KO continued raising its dividend from there, your yield on cost would continue climbing as well.

Hopefully that helps clarify things. If you'd like me to elaborate further, just reply to this email, and I'll do my best to help.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

If you haven’t already, you should check out my FREE Discord group. Think of it as one big group chat with over 3,500 dividend investors who are just as obsessed with this stuff as you are.

It’s a positive, no-drama community where people share their buys, sells, and dividend income, and talk stocks 24/7. Whether you’re just starting out or you’ve been at it for years, you’ll find people ready to answer questions, celebrate wins, and help you grow as an investor.

It’s totally free to join, and I think you’ll get a ton of value out of being part of the community.