The Hidden Force Behind Your Stock Picks

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

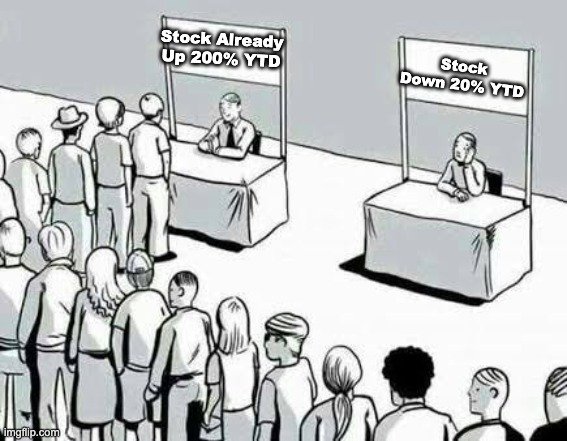

The irony of investing in the stock market is that, oftentimes, the best investing decisions in the long run are the ones that are most out of favor in the short run.

If a certain stock is down on its luck, many will question why you’re buying it when it has clearly been a “loser” based on its recent share price performance.

I see this all the time. I get comments saying, “Why would you want to buy a stock like ROL when it’s down so much this year?” Or, “Why would you want to buy VICI right now? Its share price has done nothing.”

I read those comments and think, Well, isn’t that exactly when I’d want to buy these stocks…when the businesses are out of favor and their share prices are down?

In other words, wouldn’t it be better to buy ROL at $45 instead of its recent high of $65? Wouldn’t it be better to buy VICI at $26 instead of $30, especially as a long-term, dividend-focused investor?

After all, I still think these are great businesses. Their dividends are completely intact, those dividends continue to grow, and with a lower share price, their dividend yields are now even higher than they were before.

Plus, if their share prices are already down and a lot of pessimism is already reflected in their valuations, doesn’t that put me in a better position than buying when prices are much higher?

Instead, it seems that many investors would prefer to buy stocks that are more popular and have already gone on rampant runs, like those in the semiconductor and memory spaces right now.

After all, everyone else seems to be buying them (or talking about them, at least). So isn’t that obviously a much better place to put your money?

Perhaps. Only time will tell.

Whether those stocks continue to perform well, though, isn't really the point. The point is understanding why investors are so attracted to them.

We have this innate need to fit in and to be doing what everyone else is doing. It’s safe in the herd.

That’s something deeply rooted in our evolution, and it’s something we all understand on some level, but it’s much more difficult to recognize when we’re on the receiving end of it.

This is the same reason we wear certain clothing brands, drink Starbucks coffee, and use certain slang. It feels good to fit in.

Don’t get me wrong, there absolutely can be a benefit to following the stock market crowd. Momentum investing, as this is called, has historically been a successful strategy because markets can follow a certain trend for longer than you’d think.

The problem isn’t necessarily jumping on that trend. The problem is doing so without realizing that’s what you’re doing.

There’s a difference between knowingly buying a stock because your strategy is based on momentum and blindly buying that same stock just because everyone else is buying it. The difference is whether you’re making the decision, or whether the crowd is making it for you.

In my case, it’s not easy (and it’s certainly not popular) being a dividend investor in a market that’s constantly chasing the next big thing. As time goes on, it seems that the masses are drifting farther and farther from the cash-based investing strategy I choose to pursue.

But like I said, it just comes back to knowing why you’re doing what you’re doing.

If your goal is to ride the wave of what’s hot right now and make as much money as possible as quickly as possible, then maybe a momentum-oriented strategy is a better fit for you.

But if you’re looking for an investment strategy that’s less influenced by the market’s latest obsession, then maybe this slow and steady dividend investing approach is exactly what you need.

Having said all of that, now I want to hear from you: Have you ever bought a stock that everyone else seemed to hate? If so, what was it?

Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

IN MY PORTFOLIO 📈

See my full portfolio with all of my holdings, trades, and dividends on Snowball Analytics! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

My Most Bought Dividend Stocks of 2026 (So Far)

Now that we're officially halfway through the year, these are the dividend stocks I've invested in the most so far in 2026.

CAREFULLY CURATED 🔍

📺 Inside VICI - A must-watch for all VICI shareholders. In this video, Brad Thomas sits down with CEO Ed Pitoniak to talk in-depth about the company.

🎧 Risk and Reward - In this awesome episode of the Dividend Stockpile podcast, Jeremy sits down with Ben Carlson to discuss how investors can keep a cool head in a crazy market.

📚 Terry's Thoughts - Fundsmith's latest shareholder letter has been a hot topic of discussion in the investing community. In it, Terry Smith outlines how he's changing his investment approach in response to today's momentum-driven market environment. Pretty interesting read.

SINCE YOU ASKED 💬

"Starting out with $1,000, what is your best advice to get the ball rolling?"

- Pete | YouTube

This is a great question! Whether you're starting with $100, $1,000, or even $10,000, I think the best place to start is by just investing in ETFs.

I've talked about this to death here in the newsletter, so I apologize if I'm repeating myself, but I think it makes a lot of sense to build a diversified foundation for yourself and take a more hands-off approach in the beginning.

Then, as you find your groove and become more comfortable with what you're doing, you can always add in some individual companies if that's something you're interested in.

With that said, I think one of the biggest things to understand early on is that, no matter what you choose to invest in—whether it's ETFs or individual stocks—most of the progress you make in the beginning will come from your contributions, not your returns.

That's not to say appreciation and dividends don't matter, because they certainly do. But when your portfolio is still relatively small, the compound effect isn't yet powerful enough to move the needle in a meaningful way. So the fastest way to grow your portfolio is by adding as much money to it as you can.

To put that into perspective, a 1% gain on a $1,000 portfolio is $10. That's great, but it's not going to get you very close to that first $100,000.

On the other hand, a 1% gain on a $100,000 portfolio is $1,000. That's going to get you a lot closer to the next $100,000 than the 1% gain on your $1,000 portfolio.

That's why Charlie Munger famously said that the first $100,000 is so difficult, but so important to reach. Getting to that point takes a lot of consistency and sweat equity, but once you do, the compounding effect becomes much more impactful.

This is another reason why I think it's best to start with ETFs. Spending time trying to find the "perfect" investment isn't likely to make much of a difference when your portfolio is still small.

You're much better off finding ways to shovel as much money as possible into your portfolio because, in the early years, that's what's really going to get the ball rolling.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

I love hearing from you all, and I'm always looking for feedback. How am I doing with the newsletter? Is there anything you'd like to see more or less of? Which aspects of the newsletter do you enjoy the most?

Your insights on these matters are essential in making this newsletter the best it can be. If you want to help, take a moment to share your thoughts by completing this quick form. It'll take you less than 60 seconds - guaranteed.

Thanks in advance!