10 Bad Habits That DESTROY Your Wealth

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

If you’ve been investing for any amount of time, you’ve probably picked up a few bad habits along the way. I certainly have.

Some of these habits might seem small or harmless. Some of them probably even feel like the “right” thing to do in the moment.

But over time, your habits can work against you in a pretty big way. So I wanted to put together a list of some of the most common bad habits I see investors fall into, including a few that I’ve been guilty of myself.

1. Constantly comparing yourself to other investors

Unfortunately, this bad habit doesn’t only exist in investing. This is a bad habit pretty much everywhere, and it’s only gotten worse over time with the rise of social media.

When it comes to keeping up with the Joneses, the Joneses are no longer just your next door neighbors. They’re everywhere.

Because of social media, you now have the ability to constantly compare yourself to anyone in the world, many of whom are really good at posting highlight reels of their lives (or their portfolios, in our case), which can make you feel perpetually behind, even when you’re not.

And that’s where things start to get messy because comparison doesn’t just make you feel bad. If you act on those misplaced feelings of inadequacy, it can lead to some pretty bad investing decisions as well.

If you’re not careful, it can lead you to chase higher returns in stocks you wouldn’t normally consider, which leads to taking on more risk than you should, and ultimately, giving up on your strategy before you’ve given it a fair chance to actually work.

All in all, you stop focusing on what you set out to build and what your individual goals are, and instead start reacting to what everyone else is doing. And that can totally derail your portfolio.

At the end of the day, it’s important to remember that investing is not a competition. It’s not about where you’re at compared to someone else. The only comparison you should be making is with yourself.

Are you farther along today than you were yesterday? Do you have more experience than you used to? Are you a better investor today than you were a year ago?

These are the things that matter. And at the end of the day, it’s you versus you.

2. Changing your strategy too often

Piggybacking off of the last bad habit, over the 6 years or so that I’ve been investing, I’ve seen people completely change their strategies way too often.

Typically, it’s been investors going from a dividend investing approach to then deciding that dividends are “bad,” and switching to growth because that’s what they think they should be doing.

Now, I’m all for investors doing what they believe is best. We’re all after the same thing here, so by all means, get to financial freedom in whatever way makes the most sense to you.

But the majority of the time, to be honest, I feel like a lot of this switching isn’t really coming from investors deciding that one way is bad and another way is better.

It’s not really a black and white situation like that. “Growth” and “dividends” are not mutually exclusive, and I’m telling you more about that here.

Instead, I think a lot of investors feel pressured to make the switch based on what they see other people saying online. They don’t want to be on the receiving end of criticism, so they align themselves with whatever seems to be en vogue at the moment.

Now once again, a big part of the investing journey involves evolving over time. So if that’s where your thinking takes you, then great. I’m nothing but happy for you.

But I’ll be interested to see how these same investors respond when the market isn’t so hot, and “growth” isn’t so growthy for an extended period of time.

Will they change their strategy yet again? Will they find their way back to dividend stocks? It’ll be interesting to see.

Nonetheless, at the end of the day, the best investing strategy is the one you can actually stick to. Your goal as an investor is to figure out what that looks like for you, and to be able to stick with it through the good times and the bad.

Because there will be both.

3. Not having a clear investing framework

Part of the fun of investing, I think, is turning over every rock. And that’s part of learning how to analyze stocks too. You learn by doing it, and doing it a lot.

At first, you don’t really know what you’re looking for. But after getting enough reps in, you should start to get a sense of what you’re looking for and what you think is important in an investment.

Personally speaking, I’m interested in buying companies that are growing their sales, profits, and free cash flow over time, that have the ability to still be around and relevant 10–20 years from now (low obsolescence), and that pay a dividend.

Ideally, these companies also have low (or preferably no) debt. That’s one of my favorite things to see.

Now, a lot of people will say that establishing some sort of investing framework or criteria will close you off to potentially good opportunities. And that makes sense, since any narrowing of your scope will eliminate the opportunities that exist outside of it.

But I think it’s important to have a clear sense of direction in where you’re going and what you’re looking for. You might actually be doing yourself a disservice by casting your net too wide.

Plus, at the end of the day, you only need a good 20–30ish stocks to have a complete portfolio. And I’m pretty confident that you can find at least that many opportunities within your framework.

If not, maybe your scope is too narrow, after all.

4. Researching too little (or too much)

This is a really tough one that we all struggle with. Myself included.

There have been times—especially early on—where I’ve bought a stock that I should have spent more time researching before putting money into it. 3M (MMM) comes to mind.

And there have been other times where I’ve done too much research, finding myself stuck in analysis paralysis, and missing out on a good opportunity because of it. Rollins (ROL) is the most shining example of that.

Neither is good, and you have to work at finding that sweet spot somewhere in the middle.

Fortunately, I think this gets easier over time as you develop a better sense of what you’re looking for and start to recognize the patterns that make for a good investment versus a bad one.

Still though, adding a stock to your portfolio is a big commitment. This, at least in my case, is what causes me to be too slow to pull the trigger sometimes.

My friend Russ has a way of going about this that I really like. When he finds a company he’s interested in owning, he’ll start what he calls an “exploratory position.”

This is a small starter position that allows him to get his feet wet and overcome that analysis paralysis while still getting some skin in the game.

If, after further research, he ends up liking the company, he’ll build out the position. If not, he removes it. No harm, no foul (or at least not much).

5. Ignoring the other side of the argument

One of our quirks as human beings is that we tend to seek out information that confirms our existing beliefs.

In other words, if we’re bullish on a stock, we tend to seek out bullish content. And if we’re bearish, we seek out bearish content.

We don’t naturally like to stress test our ideas. But in investing, if you’re going to be putting your money into something, it’s incredibly important to understand both sides of the coin.

Charlie Munger was a big advocate for this. One of his most famous mental models was the idea of inversion.

Instead of figuring out why a stock is a good investment, he said you should actually start by asking what could go wrong. In other words, what could actually “kill” the business.

If you ignore that side of the argument, you’re walking into an investment half-blind, and exposing yourself to unnecessary risks. These are risks that you might have been aware of (and could have avoided) if you were just open to hearing the other side.

Obviously, it’s not always comfortable to hear ideas that go against your own, but it’s essential. Plus, it’s a good reminder not to get too attached to your ideas.

At the end of the day, they’re just ideas, after all. And someone else having a different perspective isn’t a personal attack, it’s just another way of looking at things.

Sometimes, that’s exactly what you need.

6. Chasing trends and hot stocks

This is such a big problem in the stock market, and it ties back to what we were talking about earlier with keeping up with the Joneses.

If you see someone online making money with stock ABC, you don’t want to be left out, so you start buying it.

Then someone else sees you buying it, and they do the same.

Then someone else sees that, and they jump in too.

And before you know it, everyone and their mother owns stock ABC. And then, of course you should own it, because everyone else does. So obviously, it’s a good investment. (sarcasm)

That is…until stock XYZ comes along, which is now the new “it” stock of the month.

Then everyone dumps ABC and piles into XYZ. And then something else will come along after that. It always does.

The fear of missing out (FOMO) is one of the biggest sins in investing, and it’s often driven by envy. Envy is something you should do your best to avoid—in your portfolio and in all other areas of your life.

On top of that, the other problem with chasing trends is that by the time you’re hearing about that hot stock, you’re likely already too late.

It’s kind of like chasing an ice cream truck down the road. It gets tiring pretty fast, and it usually ends in disappointment.

7. Reacting to price instead of business fundamentals

It’s easy to think of stocks as just these little blips on a screen that randomly move up and down five days a week. Because of that, it’s also easy to forget that a stock represents a real, living, breathing business.

Despite what the headlines might suggest, just because the share price changes every day doesn’t mean the business does.

Stocks go down, and people panic. Stocks go up, and people get excited.

But in the short term, neither of those movements usually has much to do with the actual business. It’s just the most tangible thing we can see, so it’s easy to get attached to it.

At the end of the day, though, if you think of yourself as a business owner (which you technically are when you own stocks), you shouldn’t get too fixated on what the share price is doing in the short-term.

What actually matters are the long-term fundamentals of the business: revenue, profits, free cash flow, etc. If those are trending in the right direction over time, then the short-term share price movements that will inevitably occur along the way are just noise.

At the end of the day, the share price is not the business.

8. Obsessing over yield

I think all dividend investors are guilty of this when they’re first starting out.

It’s easy to get excited when you see a high yield, because it feels like an easy way to build up income quickly. Plus, it’s one of the easiest metrics for a beginner investor to understand.

Still, you have to take a step back and understand why the yield is high in the first place.

In some cases, like with REITs, BDCs, and MLPs, higher yields are normal. These businesses are just structured that way.

But outside of that, a high yield can sometimes be a warning sign. And one that you should not ignore.

We can look a company like Campbell’s Soup (CPB), for example.

The yield looks attractive at first glance, but it’s high because the share price is down over 40% in the past year.

And when you see that, the next question should be: Well, why is the share price down?

Looking at the fundamentals, even though revenue has been growing, earnings and free cash flow—and their respective margins—have been trending down over time.

So the business is actually becoming less profitable. And at the same time, the payout ratios are creeping up.

All of that is to say that there’s a lot more to consider than just a stock’s dividend yield. A high yield can be exciting, but it shouldn’t be the reason you buy a stock, especially if the underlying business seems to be struggling.

9. Buying stocks… and then forgetting about them

One of the nice things about being a buy-and-hold investor is that a lot of the work is front-loaded before you even add a stock to your portfolio.

Once you’ve done your initial research and learned enough about the company to feel confident owning it, a lot of the work from there becomes more about maintenance.

It’s listening to earnings calls, keeping up with the fundamentals, and generally staying aware of what’s going on with the business.

These things might sound small, and they’re not overly difficult to stay on top of, but they’re incredibly important.

Yes, as a buy-and-hold investor, you don’t need to have your head in the charts all day or be glued to a screen while the market is open. But you also can’t completely ignore your holdings either.

Part of your responsibility as an investor is making sure your original investment thesis is still intact and playing out over time. And personally, one thing I’ve learned over the years is that you actually learn more about a business after you own it.

10. Giving up too soon

This ties back to the earlier point about changing strategies too often. Another reason I think investors are quick to abandon their strategy is because they feel like things are taking too long.

One of our natural tendencies as human beings is that we want instant gratification. And it seems that tendency has only gotten stronger over time.

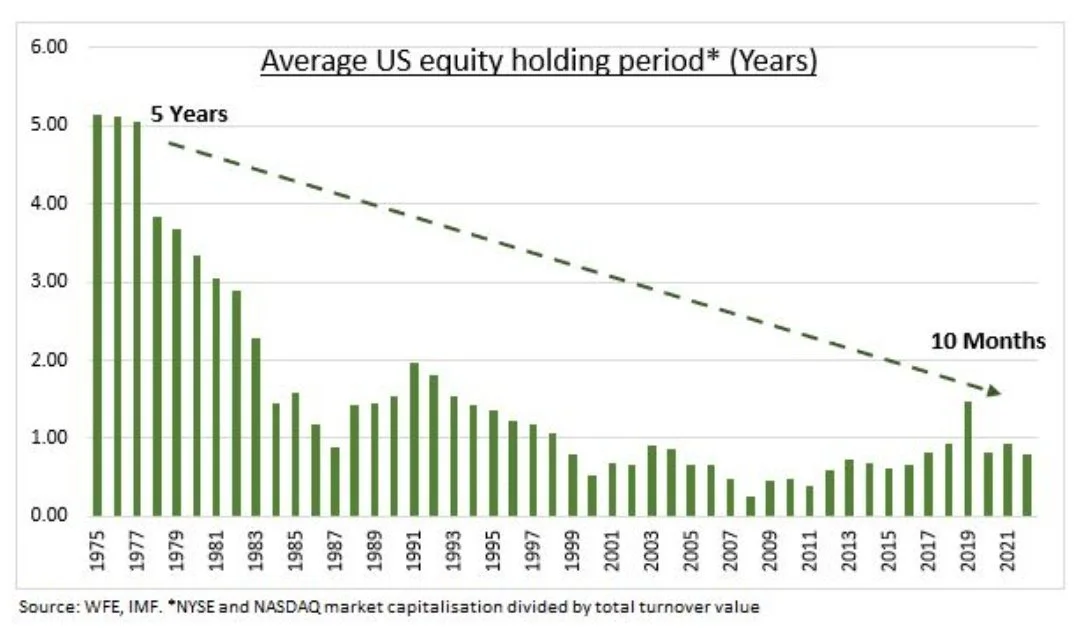

This is one of the reasons why the average holding period for stocks has dropped from around 5 years to less than a year. And it’s only going lower from here.

A lot of investors expect results in a matter of weeks or months. But the reality is, building long-term, lasting wealth takes time.

Compound interest really only works if you give it time. Time is actually the most important ingredient in the compounding equation.

The problem is, most investors either quit or change strategies before compounding ever has a chance to really kick in. And that’s where the real damage gets done.

Personally, I’m really glad that I’ve stuck with dividend investing. There’s been plenty of temptation along the way to do things differently or follow what others are doing, but sticking with it has worked out far better than I expected, and I can’t wait to see how the portfolio continues to develop over time.

Conclusion

Now that you’ve made it to the end of what I think is my longest article to date, I want to hear from you: What’s one investing habit you’ve had to unlearn over time? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

IN MY PORTFOLIO 📈

See my full portfolio with all of my holdings, trades, and dividends on Snowball Analytics! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

Inside My $130,100 Dividend Stock Portfolio | APRIL UPDATE

In this month's portfolio update, I'll do a full reveal on how my portfolio performed this past month, which stocks I bought, and what my plans are for this upcoming month.

CAREFULLY CURATED 🔍

📺 Dividends Don't Matter? - This video from GenEx Dividend Investor makes a great point that often gets lost among dividend investors: Income matters, but so do your total returns.

🎧 Timless Truths - This episode of the Richer, Wiser, Happier podcast shares timeless investing lessons from legends like Howard Marks and Nima Shayegh.

📚 Napkin Portfolios - This Substack article from Bogumil Baranowski serves as a good reminder that as your portfolio grows, the way you think about investing needs to change as well.

SINCE YOU ASKED 💬

“I recently started shifting my focus from growth stocks to undervalued dividend stocks. My dividend portfolio isn’t very large yet, but I currently have 5 individual dividend stocks that I’m consistently DCAing into. My question is: Should I be DRIPing those dividends, or just letting them build up as cash?”

- Blake | YouTube

This is a great question, and you’re definitely not the only one trying to figure this out. A lot of investors go back and forth on DRIP. And honestly, I think you can make a good case either way.

Personally, I currently DRIP all of my dividends. So everything just gets automatically reinvested back into the positions that paid them.

I didn’t always do it this way though. There was a long stretch where I let the dividends build up as cash and then manually reinvested them.

At the time, I wanted more control over how my capital was being allocated in the portfolio. I was starting to generate a decent amount of income each month ($100, $200, or more), and it felt like a meaningful amount of money that I could put toward whichever positions I was most focused on at the time.

More recently, though, I switched back to automatically reinvesting everything. I ultimately came to the conclusion that there were a lot of positions I hadn’t added to in a long time—like AbbVie (ABBV), Snap-on (SNA), and Williams-Sonoma (WSM)—and these are all businesses I really like and want to keep building.

Turning DRIP back on was a way to force myself to add to these positions again without overthinking it. It also just simplifies things since it’s one less decision I have to make when it comes to managing my portfolio.

At the end of the day, I think it really comes down to this: if you want a more automated, hands-off approach, DRIP makes a lot of sense. But if you prefer having more control over where your money goes, letting dividends build up as cash and manually reinvesting is perfectly fine too.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

If you haven’t already, you should check out my FREE Discord group. Think of it as one big group chat with over 3,500 dividend investors who are just as obsessed with this stuff as you are.

It’s a positive, no-drama community where people share their buys, sells, and dividend income, and talk stocks 24/7. Whether you’re just starting out or you’ve been at it for years, you’ll find people ready to answer questions, celebrate wins, and help you grow as an investor.

It’s totally free to join, and I think you’ll get a ton of value out of being part of the community.