I've Been Chasing This Stock For Years

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

I’ve been waiting for the opportunity to write this article for years. I’m not even joking.

For the last three or four years now, I’ve been chasing what I call my “Great White Whale.” This elusive stock has evaded me for far too long because it always seemed too expensive, which we’ll talk more about later.

If you’ve been following my YouTube channel or this newsletter for a while, then you’ll already be familiar with my Great White Whale. If not, the stock I’m talking about is Rollins Inc. (ROL), and I am proud to say that I am officially a shareholder.

In case you’ve never heard of the company before, Rollins is one of the world’s largest pest control businesses, and I’ve had a pretty interesting history with it over the years.

When I first started talking about Rollins, shares were sitting somewhere around $33-$35, and there was so much I loved about the company. Most notable is the fact that pest control is a very easy business to understand.

Things like ants, termites, cockroaches, spiders, and other critters are always going to be around. And pests are not concerned with the state of the economy, wars in the Middle East, hyperscaler cap-ex plans, or whatever other macroeconomic issue investors happen to be worrying about.

Pests are a constant. And people will never want them invading their homes or businesses, and that’s what makes Rollins such an attractive and timeless investment.

In a constantly changing world, the bull case for Rollins is rooted in a constant that will probably never change. And that predictability shows up in the numbers.

Source: Fiscal.AI

Around 75% of the company’s revenue comes from recurring service agreements, which have helped fuel years of steady and consistent growth.

The company also keeps a squeaky clean balance sheet, giving it plenty of opportunity to continue growing through acquisitions. That’s another thing I like about Rollins.

The pest control industry remains very fragmented, with tens of thousands of local operators spread throughout the country. Rollins regularly acquires these smaller pest control businesses and provides them with the resources, technology, and scale that come with being part of a much larger organization.

Over time, these acquisitions help expand Rollins’ geographic footprint while creating additional opportunities for growth, which the company refers to as “multiple bites at the apple.”

All in all, I think there’s a lot to love about this company. The problem with it is that everyone else seems to think so too.

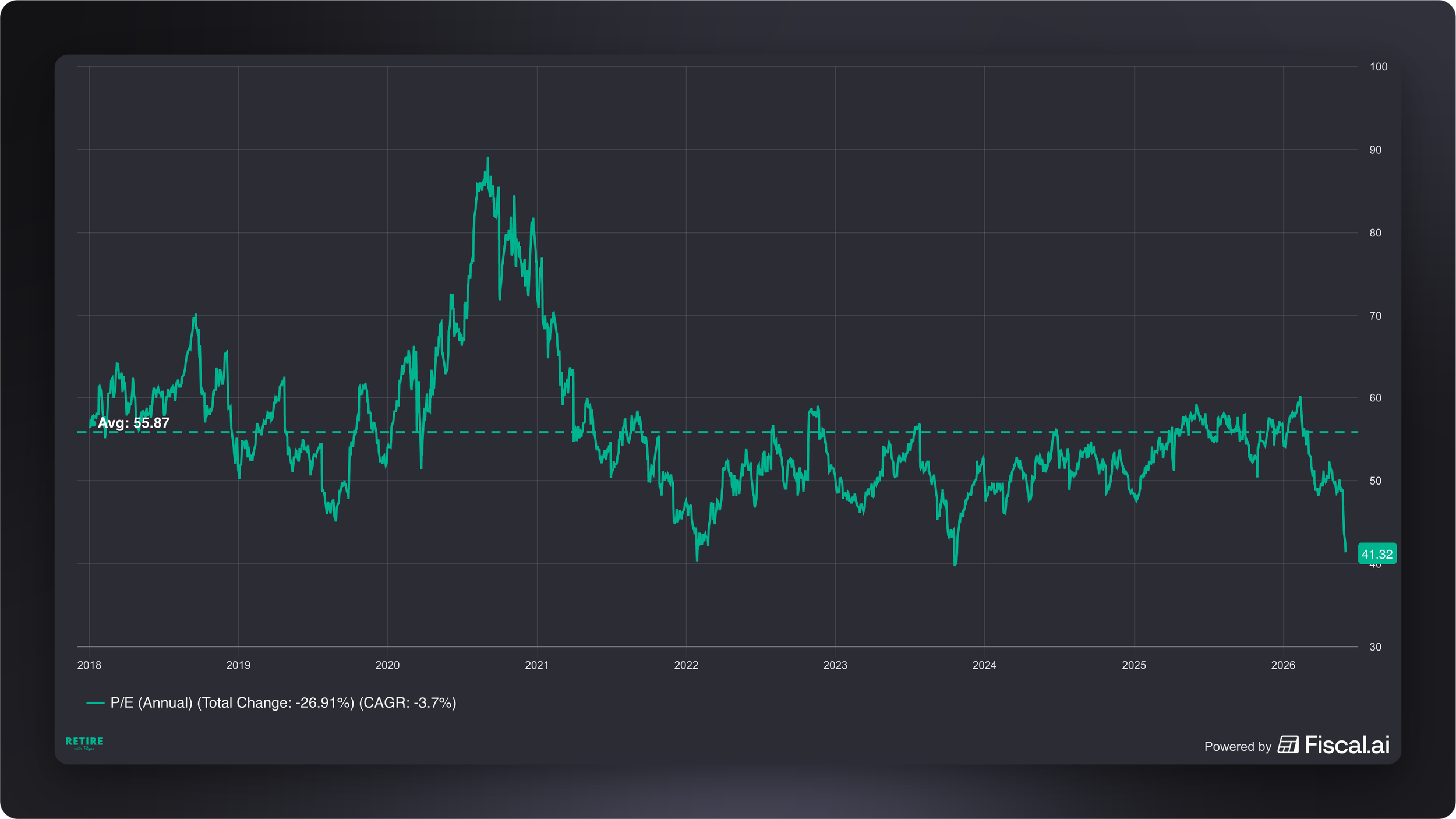

Source: Fiscal.AI

Over the past decade, Rollins has traded at an average P/E ratio of about 56. That’s the type of valuation you’d expect to see from a hyper-growth tech company, not one that sprays your house for bugs.

And that’s what kept me from owning this company for years. Every time I looked at Rollins, I couldn’t help but think it was just too expensive.

Source: Fiscal.AI

Only after seeing the share price hit a peak of $65 per share earlier this year, though, have I been able to see how dumb it was for me to pass on the company in the $30s. As they say, yesterday’s peak is tomorrow’s trough.

Since the start of the year, though, Rollins has finally given wannabe shareholders like myself a bit of hope. The share price has (thankfully) pulled back into the mid-$40’s, and while the valuation is still far from cheap with a P/E of about 41, it’s considerably more reasonable than it was a few months ago.

Seeing that opportunity, I decided that now was probably a decent time to start a position. I’m taking it slow, though.

So far, I’ve only purchased 39 shares at an average cost of $49.25 per share, and with the position currently making up only about 1.2% of my portfolio, I have plenty of room to add more over time.

Ultimately, I’d like Rollins to become a 5-6% position before I hit the pause button on buying. But since the share price doesn’t seem to have found its bottom yet, I’m not in too much of a rush to build this out too quickly.

The biggest risk, as I see it, is still the valuation. Even after the pullback, this isn’t what most people would consider a cheap stock.

But after spending years chasing this company, I’ve come to appreciate another risk that, in my experience, often gets underestimated: the risk of never owning a great business because you’re waiting for the perfect price.

For years, Rollins was my Great White Whale. Now it’s finally part of my portfolio, and I’m excited to be able to focus on building out this position in the coming weeks and months at what seems to be, at least, a reasonable valuation.

Anyway, enough about me. Now I want to hear from you: What was the most recent stock you added to your portfolio? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

Blossom is a unique social platform created by investors, for investors. Unlike the usual social media platforms, Blossom is dedicated exclusively to discussions on finance and investing.

I've been actively posting on Blossom for a few years now and I absolutely love the community on there. With over 400,000 DIY investors, Blossom is buzzing with all sorts of different investment ideas. The coolest part is that you can see everyone's full portfolios (including mine), which you can automatically link within the app!

Picture Twitter/X, but with an added portfolio tracking feature and less trolling – that's Blossom for you. Personally, I find it much more enjoyable than my experience on Twitter/X, and I think you will too.

Download Blossom today, and follow me (@ryne) to see my entire portfolio and stay updated on all my real-time investment moves.

IN MY PORTFOLIO 📈

Start tracking your portfolio with Snowball Analytics today—free for 14 days! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

3 DEEPLY Discounted Dividend Stocks To Buy In June

In this video, we'll go over 3 discounted dividend stocks that seem like good buys right now as we jump into June.

CAREFULLY CURATED 🔍

📺 The Golden Goose - This video from Toby Mathias was of the better explanations I've heard for why some investors prioritize cash flow over capital gains.

🎧 Fever Dream - Russ just had a great conversation with our friend Jonah Weingarten about his portfolio, which is built almost entirely around high-yield, covered call ETFs and pays daily dividends.

📚 Words Matter - Daniel Peris dives into the evolution of terms like "private equity" and "shareholder returns," arguing that the language of finance has moved away from business fundamentals and toward financial engineering.

SINCE YOU ASKED 💬

"Is SCHD still a good long-term investment in 2026, considering current market conditions, dividend performance, and growth potential?"

- Kabir | Blossom

In my personal opinion, I really think it just depends on what you're looking for in an investment.

As we look across the market right now, there is no shortage of stocks seeing astronomical returns. Names like Micron (MU), Sandisk (SNDK), and Rocket Lab (RKLB) immediately come to mind. If that's the type of investment you're looking for, SCHD probably isn't going to be a great fit.

Source: Fiscal.AI

With that said, SCHD is no slouch when it comes to returns. The fund is up close to 20% year-to-date, which is quite a bit ahead of the S&P 500 so far this year.

When you zoom out though, the S&P 500 has outperformed SCHD by a pretty wide margin since SCHD's inception back in 2011. To be fair, most of that outperformance has really occurred since 2023, during a period when the market has been largely driven by the Mag-7 and other tech/AI-related stocks.

I also don't necessarily see that underperformance as a flaw. SCHD wasn't designed to be the S&P 500.

It's purposefully built around a different type of company and different goals. Comparing the two is helpful, but I don't think SCHD needs to beat the S&P 500 in every environment to be considered a good investment.

It will be interesting to see how the two compare during the next extended downturn, which is something we really haven't experienced since I started investing in 2020.

Because of the nature of the companies SCHD owns, which are businesses that tend to be highly profitable and have a track record of paying and growing dividends, I would expect SCHD to hold up a bit better than the broader market during tumultuous times.

Source: Fiscal.AI

Overall, I still think SCHD is a great long-term investment. The types of companies it holds are exactly what I'm looking for. At the end of the day, companies can't consistently pay and grow their dividends without strong underlying fundamentals.

Plus, with a yield of around 3.2% and a dividend growth CAGR at around 9%, SCHD has some of the best overall dividend stats out there. In my portfolio, it plays the role of the steady dividend grower, and it does that job very well.

Because of that, I actually think it pairs nicely with an S&P 500 fund. The S&P clearly has more of an advantage on the appreciation side of things, while SCHD brings a stronger income component to the table.

There also isn't a ton of overlap between the two, which is why I think it's completely reasonable to own both and let them complement one another.

Have a question? Ask me here to see it featured in an upcoming newsletter.