The Next Two Dividend Milestones I'm Chasing

PRESENTED BY SNOWBALL ANALYTICS

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

In my experience, dividend investing is both a “slow burn” and it’s also “the gift that keeps on giving.”

Chances are, you’re not going to see your portfolio of dividend stocks blow up overnight (in either sense of the phrase). On the contrary, it takes a long time to amass a massive amount of wealth with this style of investing, which is why it’s a “slow burn.”

Despite that, it does get better the longer you do it. While your dividend payments may only be a few cents here or a few dollars there at first, it doesn’t take as long as you think before they start adding up to an amount of income that can actually pay for some real-life things.

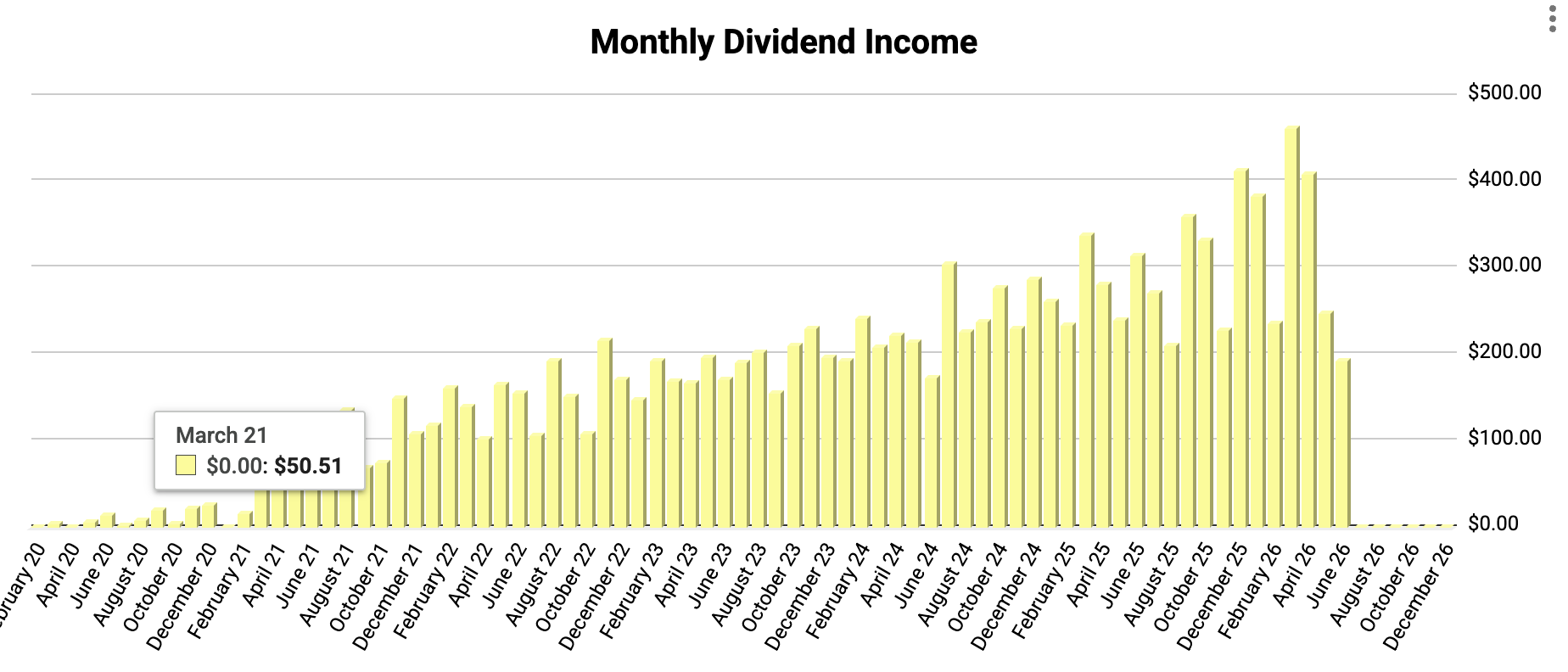

In my case, it only took around eight or nine months before I had my first $50 month of dividends. Obviously, $50 isn’t a life-changing amount of money, but think of all the things that it could pay for.

More important than the money itself is what it represents. That small, but growing stream of income is proof that what you’re doing is working.

And the longer you do it, the larger those payments become and the faster they grow. That’s why dividend investing is also “the gift that keeps on giving.”

Still, because it is so slow to gain steam, especially at the start, one of the most difficult parts of being a dividend investor is being patient and trusting the process enough to stick with it.

This is especially true when there are so many other shiny objects in the stock market begging for your money, and so many other people who seem to be growing their wealth faster than you.

One of the things that has helped keep me from chasing these shiny objects over the years is celebrating the small victories along the way. Your first $100 month. Your first $1,000 year. Getting to the place where you’re averaging $100, $200, or even $300 per month in dividend income.

Like I was saying earlier, none of these milestones will allow you to retire. But they are still worthwhile because they serve as evidence that you’re on the right path. Progress is being made.

I think it’s important to keep tabs on these milestones along the way. No matter how big or small, there’s a sense of accomplishment that comes with hitting these nice, round-number landmarks in your dividend investing journey, and they give you something exciting to work toward.

That brings me to the two dividend income milestones I’ve got my eyes on right now.

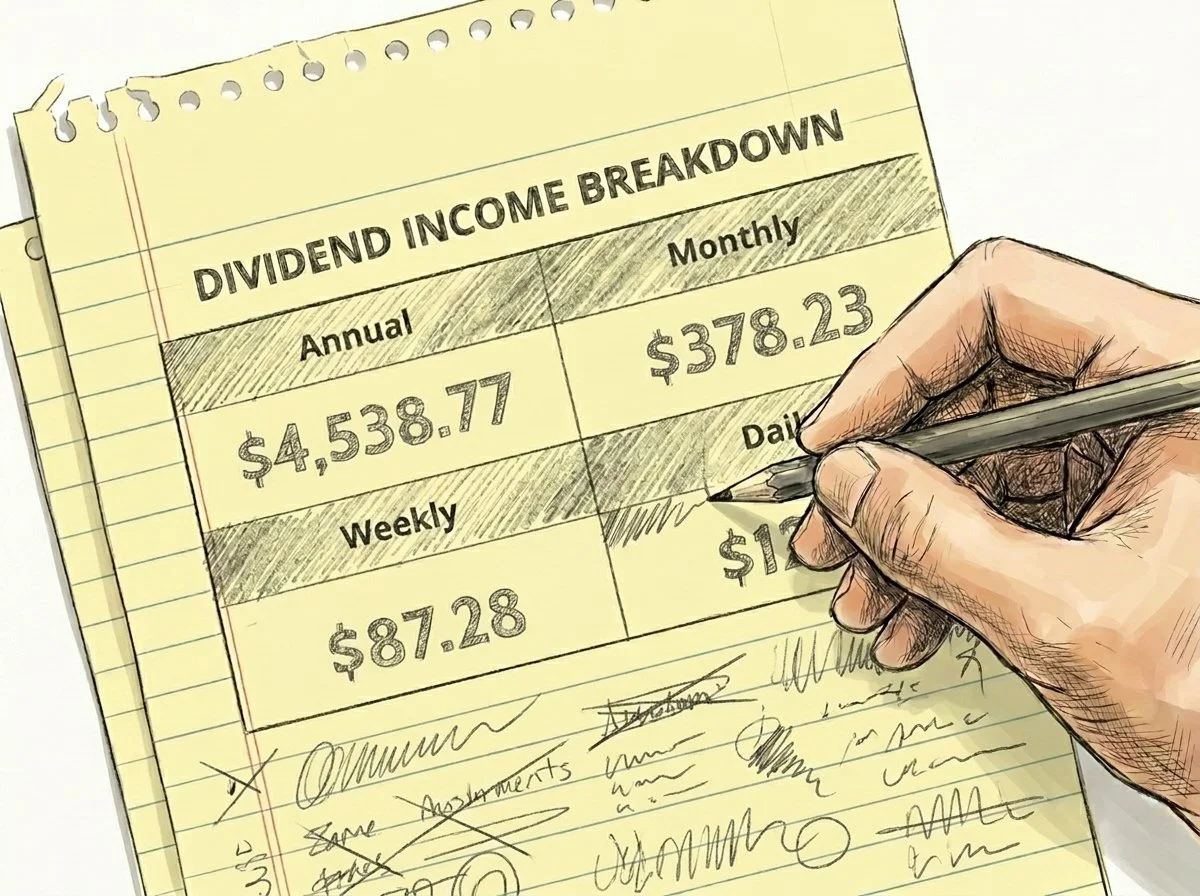

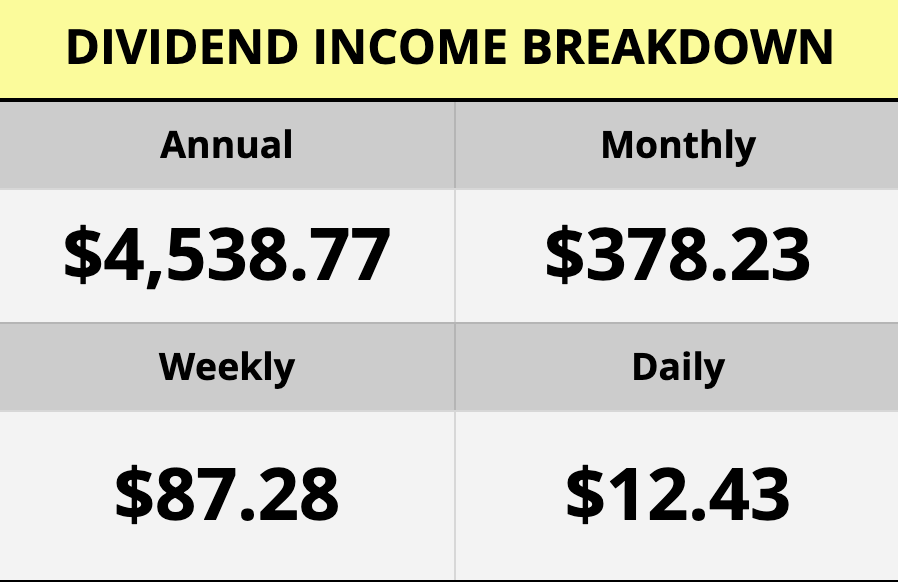

The first one is right around the corner, and that’s getting to a point where I’m averaging $400 per month in dividend income ($4,800 per year).

Right now, I’m less than $22 per month (or about $262 per year) away from hitting that goal, and I should hopefully be there by the end of the year. Running the numbers, if I continue investing at my portfolio’s overall dividend yield of 3.3%, I’ll need to invest another $7,939 to reach that target.

Since I’m investing an average of about $1,274 into my combined accounts every month (not including my wife’s brokerage account, which is actually receiving more contribution dollars per week than mine), reaching this goal should take another six months or so.

Of course, that timeline doesn’t include dividends being reinvested or any dividend increases that will inevitably occur along the way, so it will almost certainly happen a bit sooner than that. Thank goodness.

The second goal, though, will definitely take a bit longer to reach. This one is reaching $100 per week in dividend income ($5,200 per year), and I’m currently about $13 per week (or about $662 per year) away from hitting it.

Investing at that same average portfolio yield of 3.3%, I’ll need to invest another $20,060 to get there. And at my current contribution rate, that should take around 16 months, which means I’ll hopefully reach that milestone sometime around October of next year at the latest.

Now, as much as I’d love to be there tomorrow, and as far away as 16 months may sound, I have to remind myself of the “slow burn” nature of this whole thing. The reality is that there are no shortcuts to building long-term wealth.

Still, when I first started investing back in 2020, I never imagined I’d be bringing in almost $400 per month just a few short years later. That’s the great thing about dividend investing though: those round-number landmarks seem impossibly far away, but before you know it, you’re staring them right in the face.

All you have to do is get started and just keep going. Easier said than done, of course, but that's really the secret.

Anyway, enough about me. Now I want to hear from you: what dividend investing milestone are you currently working toward Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

One of the most essential tools for any investor is a reliable portfolio tracker, and Snowball Analytics is the ultimate command center for your portfolio, providing all the tools you need (and more) in one place.

Plus, it’s one of the only portfolio trackers out there designed specifically for dividend investors.

The layout is clean and intuitive, offering charts, graphs, and other features you didn’t even know you needed but now can’t live without—like the dividend calendar, portfolio backtest tool, and the dip finder tool (this has been a game changer).

I’ve been using Snowball for a couple of years now, and it's the most in-depth portfolio tracker I’ve ever used (you can see my entire portfolio on Snowball here). I highly recommend it to any dividend investor looking for maximum functionality and data for tracking their portfolio.

Right now, Snowball Analytics is offering a 14-day FREE trial so you can try it out risk-free. The best part is, if you end up loving it (which, as you'll find out, is not hard to do), you can save 10% on your subscription when you use code “rynewilliams” upon signing up.

IN MY PORTFOLIO 📈

See my full portfolio with all of my holdings, trades, and dividends on Snowball Analytics! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

I’ve Been Chasing This Stock For Years (and FINALLY Bought It)

I finally bought my "Great White Whale" dividend stock. In this video, I'm breaking down all the details.

CAREFULLY CURATED 🔍

📺 Dividends Aren't Dead - There's a growing narrative that dividend investors are being left behind by AI, but Gen Ex Dividend Investor makes a great case for why dividend investing is still very much alive and well.

🎧 Let Your Winners Run - Mohnish Pabrai joins the We Study Billionaires podcast to talk Berkshire Hathaway, investing mistakes, and the importance of letting your winners run.

📚 The New Google - Ben Thompson from Stratechery breaks down how AI is changing Google's business model, and why deep pockets might be the ultimate competitive advantage in the next era of technology.

SINCE YOU ASKED 💬

"When you start a position in a new company and the stock immediately starts falling, how do you know when it's the right time to buy more? What if the stock just keeps going down?"

- JD | YouTube

This is a great question. And believe it or not, if you're building out your position in a company, one of the best things that can happen is for the share price to go down after you buy it (assuming nothing has fundamentally changed about the business, of course).

I actually have some recent experience with this from the addition of Rollins (ROL) to my portfolio. I started a small position around $49 per share, and pretty much immediately after, it fell to around $45.

Rather than taking that as a bad thing, I welcomed it. After my small, initial tranche, my plan was to gradually build out my position over time. To me, a lower share price just meant I could buy more shares with the same amount of money and lower my average cost per share along the way.

It also meant I was locking in a higher dividend yield. Since the yield is calculated relative to the current share price, buying at a lower price means you get a better cash-flow return on your investment. As the share price goes down, the dividend yield goes up.

Now to directly answer your question, you never really know if you're buying a stock at exactly the right time. Nobody knows where a stock will ultimately bottom out before it starts making its ascent again.

But if you're buying a high-quality company because you believe it will be worth more at some point in the future, then lower prices along the way are generally something to be excited about, not afraid of.

I wouldn't get too fixated on trying to time it perfectly. As long as your original investment thesis remains intact, lower prices are simply an opportunity to buy more shares at a discount.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

I love hearing from you all, and I'm always looking for feedback. How am I doing with the newsletter? Is there anything you'd like to see more or less of? Which aspects of the newsletter do you enjoy the most?

Your insights on these matters are essential in making this newsletter the best it can be. If you want to help, take a moment to share your thoughts by completing this quick form. It'll take you less than 60 seconds - guaranteed.

Thanks in advance!