My Top Dividend Stock To Buy In March

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

One thing you can count on in the stock market is that there is never a dull moment.

Between AI disruption concerns, ongoing geopolitical tensions, and now the re-ignited chaos surrounding tariffs, share prices don’t seem to know which way to go. And lately, many of them have been heading lower.

On one hand, it doesn’t feel good to see your gains getting wiped out. That’s completely understandable. But on the other hand, what a great time it is to be buying stocks!

With all the craziness swirling around, plenty of high-quality, cash-printing companies are going on sale. Especially in the tech and software space, where the buying opportunities seem to be getting better by the day.

Because the future impacts of AI are so uncertain, some of the decline in tech is deserved. Some of it, maybe not so much. I talked all about that in a recent video.

It seems to me that quite a few companies have become collateral damage, and in my opinion, Visa (V) falls into that category more than anything else. That’s why it’s my top dividend stock to buy in March.

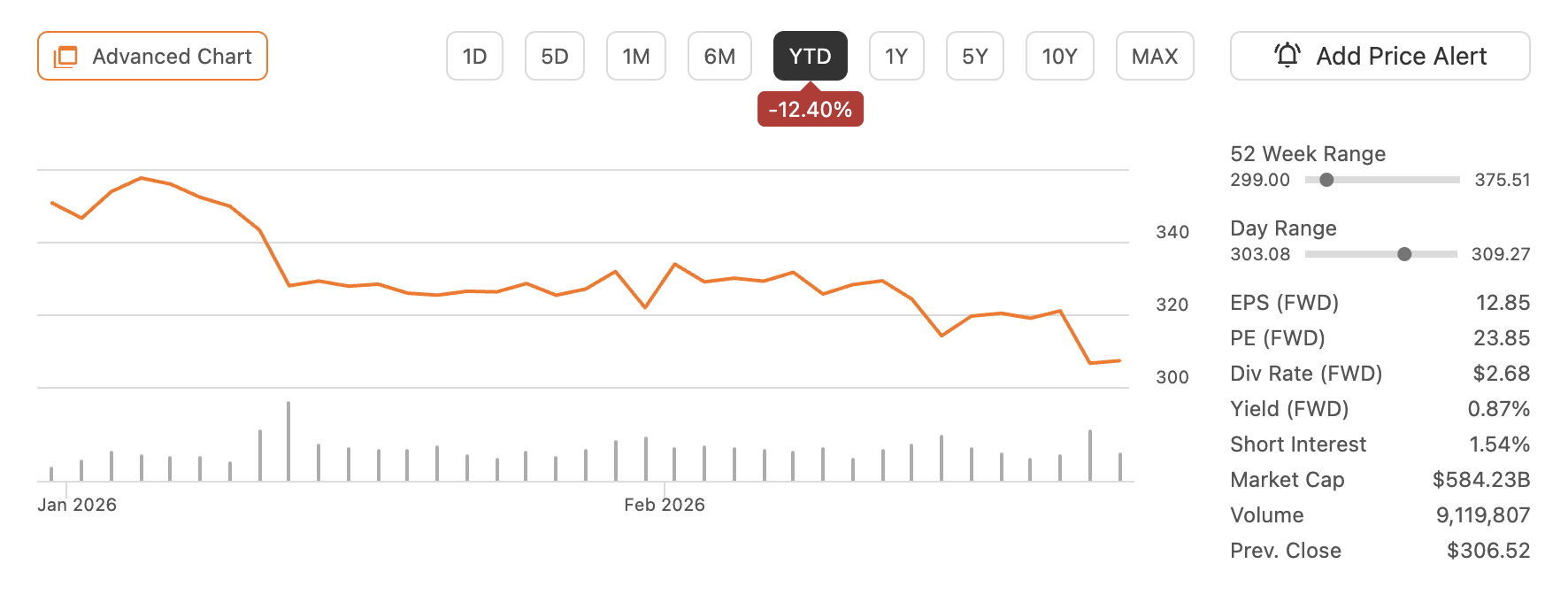

Over the past month alone, Visa’s share price has declined roughly 6%, and it’s now down about 12.4% year-to-date — falling from around $350 at the start of the year to now hovering near $300 per share.

At this rate, I wouldn’t even be surprised if we see it dip below $300. I would not mind that at all, either.

Source: Seeking Alpha

For a company of such high quality, a drop like that makes you stop and wonder: what exactly is going on? And from what I can see, there are a few catalysts putting pressure on the share price right now.

First, as already mentioned, there are the broad concerns around AI disruption and what that means for tech-heavy companies moving forward. It’s on everyone’s mind at this point, as I’m sure you’ve noticed.

Because Visa is a large-cap, tech-heavy name (despite technically being classified in the financials sector), it’s getting caught in the crossfire.

As money rotates out of tech and into more defensive names (like CAT or MCD, which have been on fire lately), companies like Visa don’t get spared, even though its business model looks nothing like the software companies currently center stage in all of this.

Second, and more specific to this month’s pick, Europe has begun pushing for reduced reliance on U.S.-based payment processors like Visa and Mastercard (MA).

According to the European Central Bank, Visa and Mastercard accounted for nearly two-thirds of card transactions in the Eurozone in 2022. That level of dominance has raised concerns (not for the first time, either) among European officials about strategic dependence, especially in a world where geopolitical tensions have proven they can escalate quickly.

In response, the European Payments Initiative (EPI), an alliance of 16 European banks and financial institutions, has launched a payment alternative called Wero. It already has over 43 million registered users and is live in several countries, including Belgium, France, Germany, and the Netherlands.

More recently, multiple European payment providers signed a memorandum of understanding to accelerate the rollout of a sovereign, cross-border European payments system by 2027. There’s even discussion of a digital euro, although that may not arrive until 2029.

Now, this is all actually happening as we speak. It’s not just talk.

But my opinion is that even if this initiative gains traction (and it still has a long way to go before it’s truly competitive with Visa and Mastercard), Europe represents just one region where Visa operates.

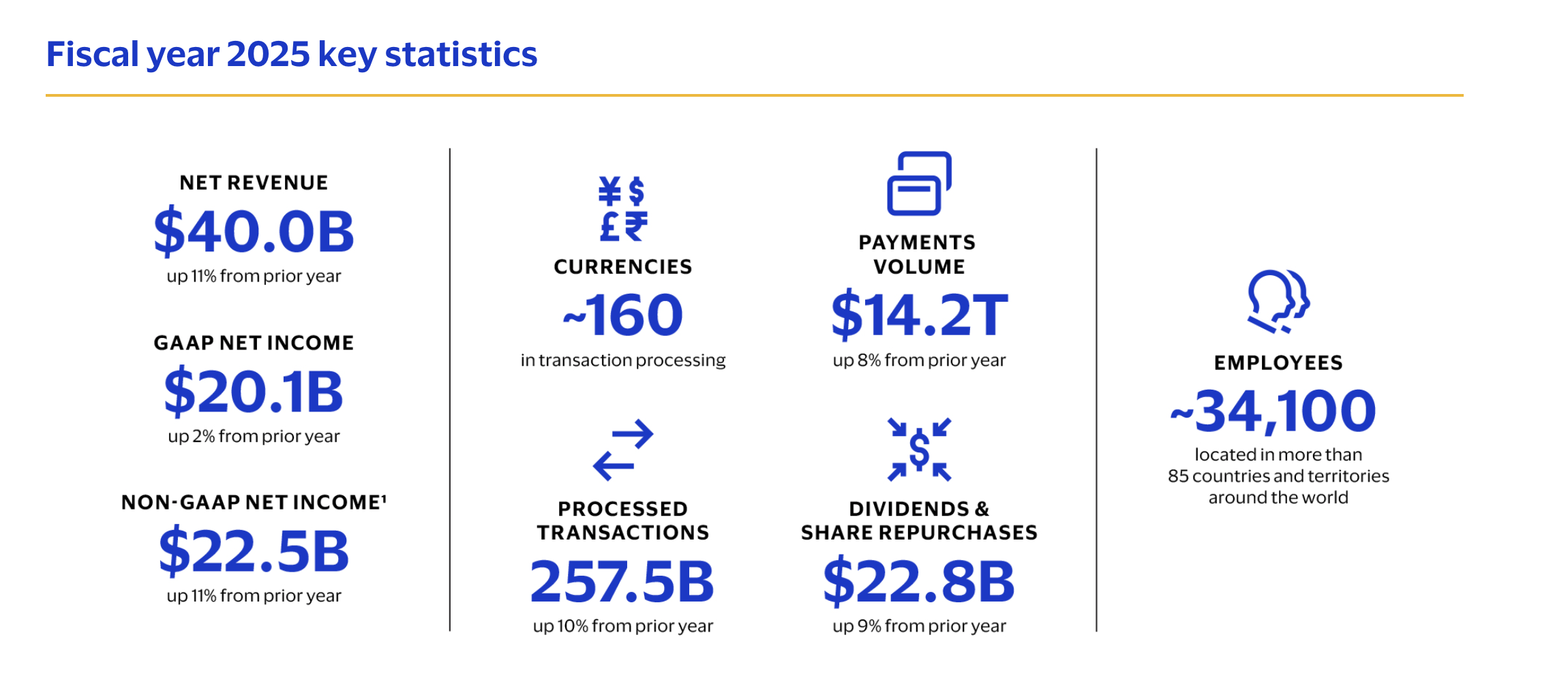

Visa has its hands in the plumbing of commerce all around the world. It operates in roughly 160 currencies, and in 2025 alone, the company processed 257.5 billion transactions and facilitated over $14 trillion in payments volume.

In other words, its network effects are enormous.

Source: Investor Relations

For this European initiative to meaningfully displace Visa, it won’t be enough to simply build a new app or domestic card system.

You would need a globally accepted, cross-border network with widespread merchant adoption, fraud detection infrastructure, issuing relationships, regulatory approvals, competitive fee structures, multi-currency support, and decades of built-in trust (which is the hardest thing to replicate). And it would all have to be done meaningfully better than Visa.

Could this become a problem over time? Possibly. After all, David did defeat Goliath.

But dethroning the company that rules global payments infrastructure is a far taller order than the headlines suggest. I think the risk of it actually happening is pretty low. So far, at least.

In the meantime, I think Visa will continue doing what it has always done: consistently grow. I’ve referred to Visa as the Gold Standard of stocks before, and the long-term growth chart really speaks for itself.

Source: Snapstock

On the dividend side, the recent pullback has pushed Visa’s yield up to roughly 0.85%. That’s not a high yield by any means, but it is about 15% higher than the company’s five-year average yield of 0.73%.

More importantly, Visa has raised its dividend every single year since going public in 2009, growing it by roughly 15% annually over the past five years. And with a payout ratio around 20%, the dividend remains extremely well covered.

Source: Seeking Alpha

Beyond the potential competition risk coming from Europe, I don’t see a life-threatening catalyst that would impair the business model anytime soon. If anything, the continued global shift toward digital payments should further strengthen Visa’s already powerful network effects.

And I’m putting my money where my mouth is with this one.

Since the start of the year, I’ve added nearly five shares to my Visa position, and I plan to continue adding more as the share price pressure persists (and hopefully worsens) in the short term. The lower the price, the more I’ll buy.

With that said, Visa isn’t the only good buying opportunity on the market right now. There are quite a few others worth paying attention to — and I want to hear from you: which discounted stocks do you have your eye on as we make our way into March? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

IN MY PORTFOLIO 📈

Start tracking your portfolio with Snowball Analytics today—free for 14 days! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

How To Become Financially Dangerous

In this episode of The Deep End, we explore the difference between innovators, imitators, and idiots, and why the direction you’re compounding determines everything else in life.

CAREFULLY CURATED 🔍

📺 Guaranteed Returns? - Chuck Carnevale from FAST Graphs explains why dividend growth investing can stack the odds heavily in your favor over time. He calls it "the closest thing to guaranteed success."

🎧 Non-Consensus Investing - Rupal Bhansali, author of the book Non-Consensus Investing (which I highly recommend), joins the Investing By The Books podcast to talk about how investment success is built on deep research, not following the crowd.

📚 Less Is More - James Emanuel dives into a study from Fidelity showing that the accounts left untouched (often because the owners had passed away) beat the ones that were actively managed.

SINCE YOU ASKED 💬

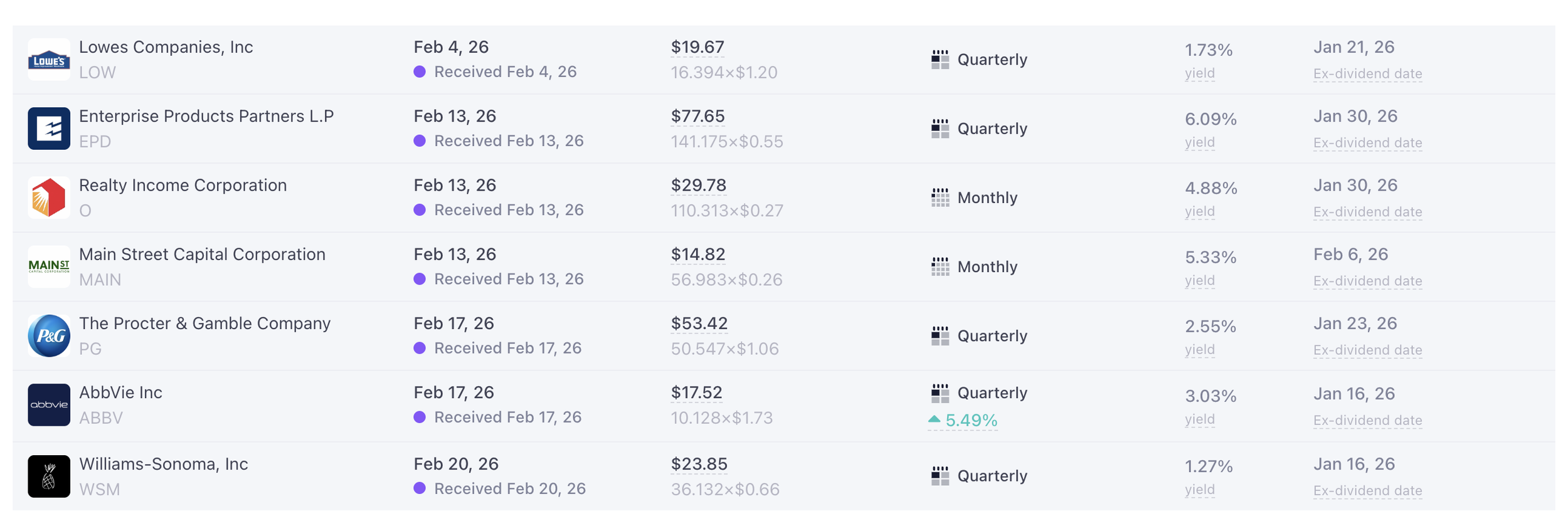

"What is your favorite stock that pays a dividend in February?"

- Bartexoon | YouTube

Out of the three months in the quarter, February is the lightest month of dividend payments for me. You can see all of this month’s payments below.

Source: Snowball Analytics

With that said, I wouldn’t get too hung up on which month a company pays its dividend.

I know plenty of people like the idea of perfectly balanced dividend income every single month, and I don't blame them. But that should always come secondary to the investment itself.

In other words, you shouldn’t give a company extra brownie points just because it pays in a specific month or because it pays monthly instead of quarterly. The quality of the business and its ability to grow its dividend over time are much more important than the timing of the payment.

Plus, if you own a diversified portfolio of dividend-paying companies, it’s pretty difficult not to end up with payments naturally coming in every month. You really don't have to go out of your way to achieve that.

The payments might be a little lumpy month-to-month, but it all evens out in the end.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

If you haven’t already, you should check out my FREE Discord group. Think of it as one big group chat with nearly 4,000 dividend investors who are just as obsessed with this stuff as you are.

It’s a positive, no-drama community where people share their buys, sells, and dividend income, and talk stocks 24/7. Whether you’re just starting out or you’ve been at it for years, you’ll find people ready to answer questions, celebrate wins, and help you grow as an investor.

It’s totally free to join — and I think you’ll get a ton of value out of being part of the community.