My Top Dividend Stock To Buy In May

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

Like most months, April had its fair share of ups and downs. But unlike last month, this one leaned much more toward the upside, with the S&P 500 delivering about a 9% gain.

That’s great news if you’re looking to get out of the market on a high note. But if you’re still a regular buyer of stocks—as I’m sure many of us are—it’s actually the opposite of what you’d want to see.

Fortunately, even as the broader market moves back up, there are still a handful of stocks that choose to zig while the market zags.

One such opportunity is Badger Meter (BMI)—a stock I’ve talked about pretty regularly on the channel and here in the newsletter, and my top dividend stock to buy in May (you can check out some of my other top stock picks here).

I think Badger Meter is a bit of a hidden gem in the world of dividend investing. I really wish more people were talking about this company because it’s great.

In a nutshell, BMI makes water meters and sensors that help cities and businesses track how much water people are using. And while that might not sound all that exciting at first, the company has quietly evolved from a traditional hardware manufacturer (established in 1905) into a key player in digital water metering.

Through its BlueEdge platform, Badger provides tools that allow municipalities to monitor the entire “full water cycle”—everything from drinking water to sewer systems and even leak detection.

The interesting part is that because the hardware is paired with software, Badger has been able to build a growing stream of recurring revenue while also embedding itself deeply into its customers’ workflows.

Once these systems are in place, they’re not easily swapped out. Replacing them would essentially mean ripping out the entire nervous system of a local water utility.

I think a lot of people hear “water meters” and immediately write this one off as some boring, sleepy business. But in reality, Badger is working with some pretty advanced technology, and water is something we all depend on at the end of the day—so it’s a pretty important business too.

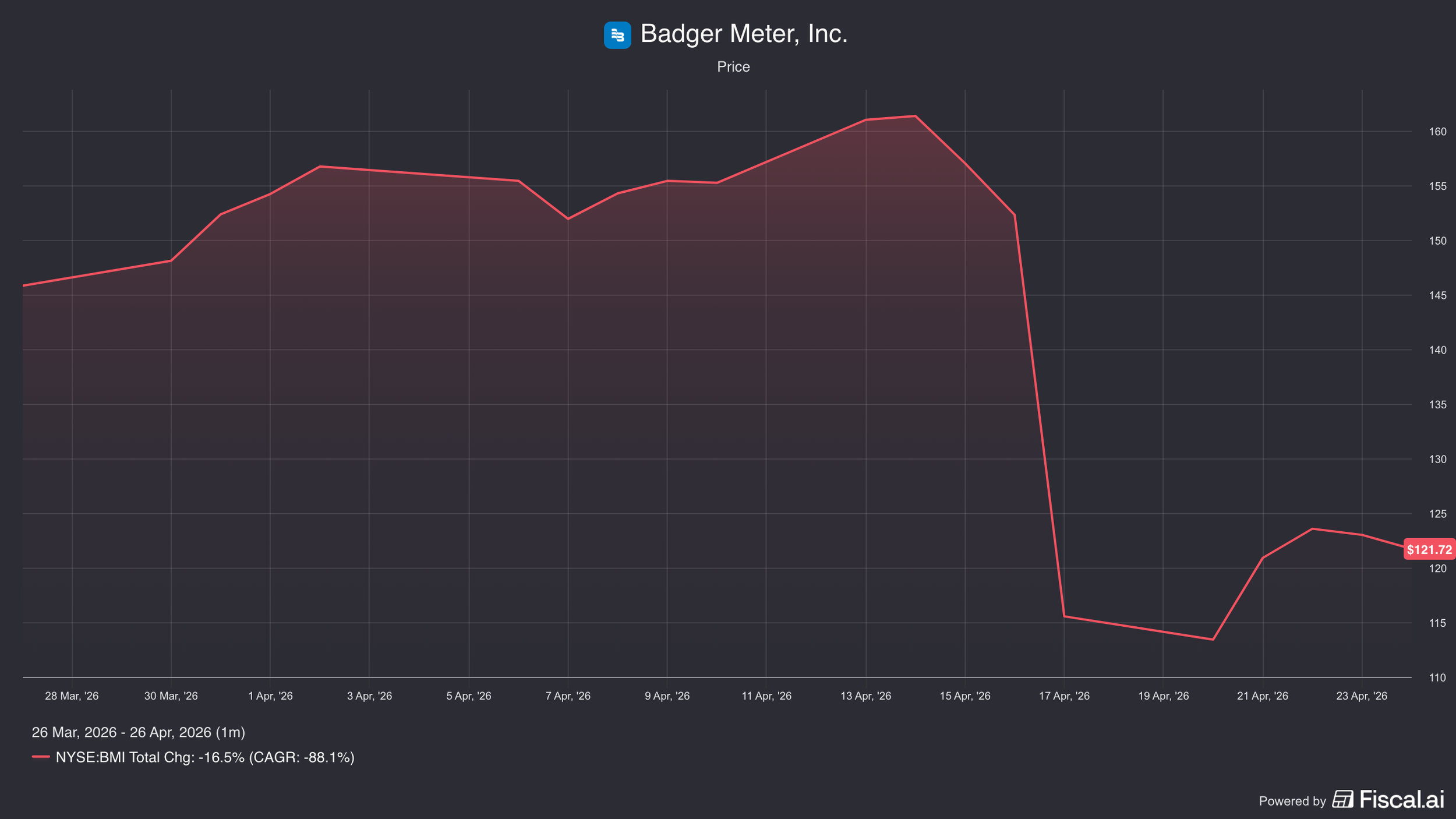

Source: Fiscal.AI

With that said, Badger Meter’s share price has clearly fallen on hard times. As we can see from the chart above, the stock is down 16.5% over the past month and about 43.6% over the past year.

If you look closely, there’s a pretty sharp drop in the middle of the month, and the main catalyst for that was the company’s latest earnings report.

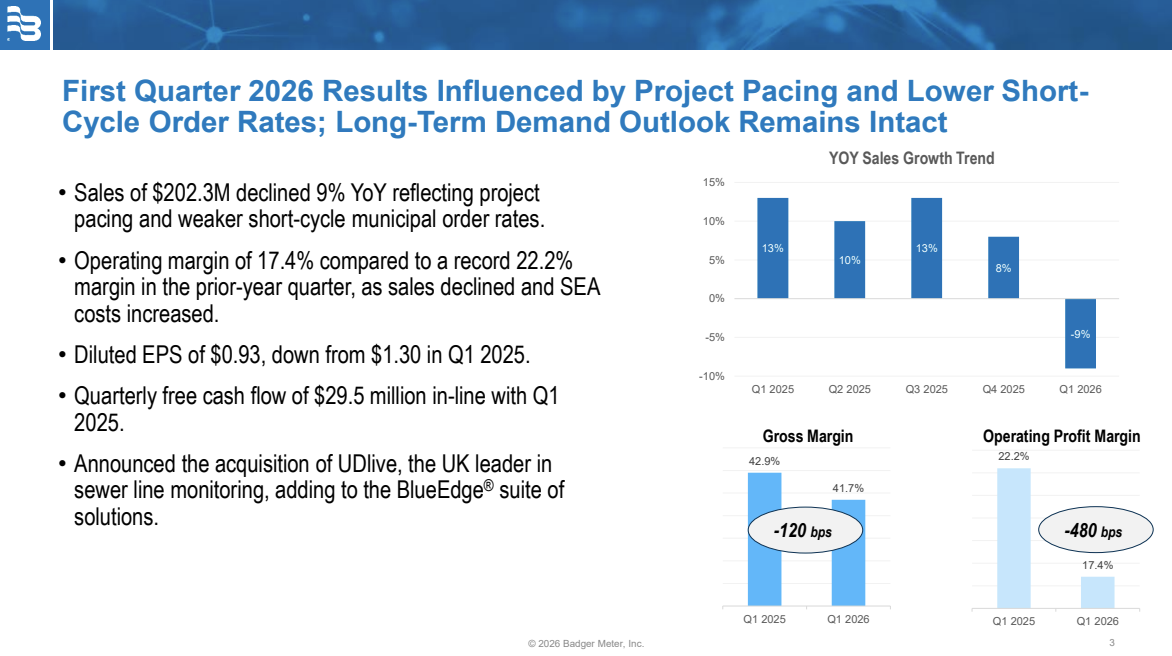

Source: Fiscal.AI

Looking at the numbers (which you can pull up right within Fiscal.AI), sales for the quarter were down 9% year-over-year, and EPS took a hit as well. Fortunately, free cash flow was on par with last year, so at least there’s some stability there.

Now, on the surface, that kind of decline might sound pretty concerning. But on the earnings call, management explained that this was largely a timing issue.

Source: Fiscal.AI

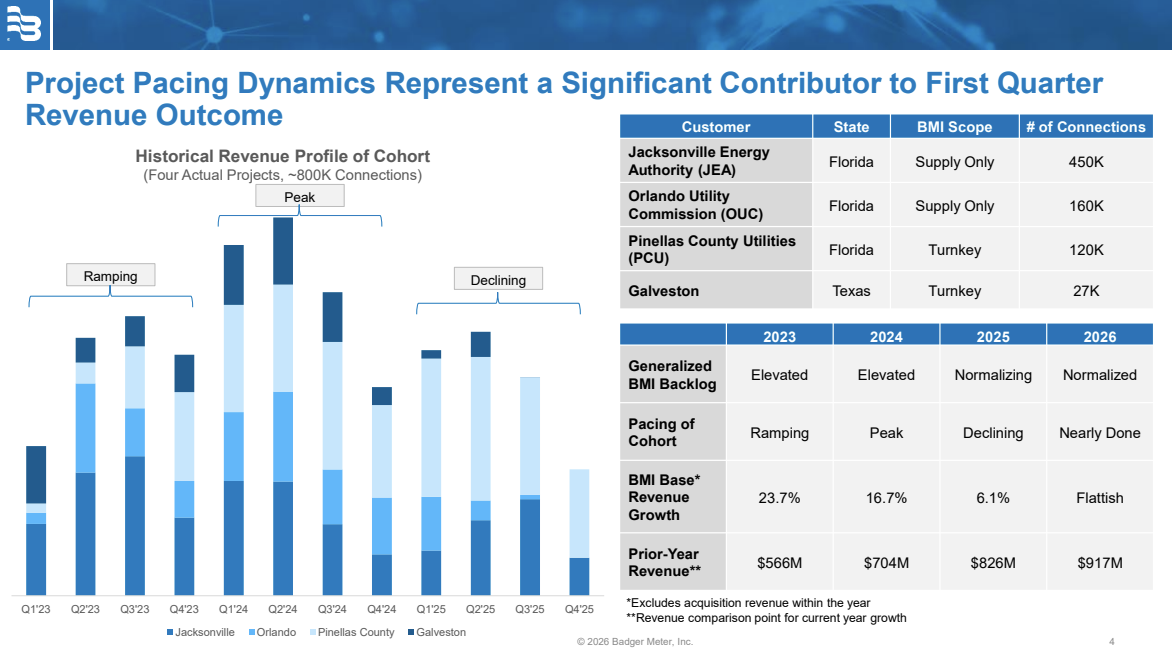

Over the past few years, Badger has been working on a group of four massive water projects. By the start of this year, those projects were wrapping up and nearing completion.

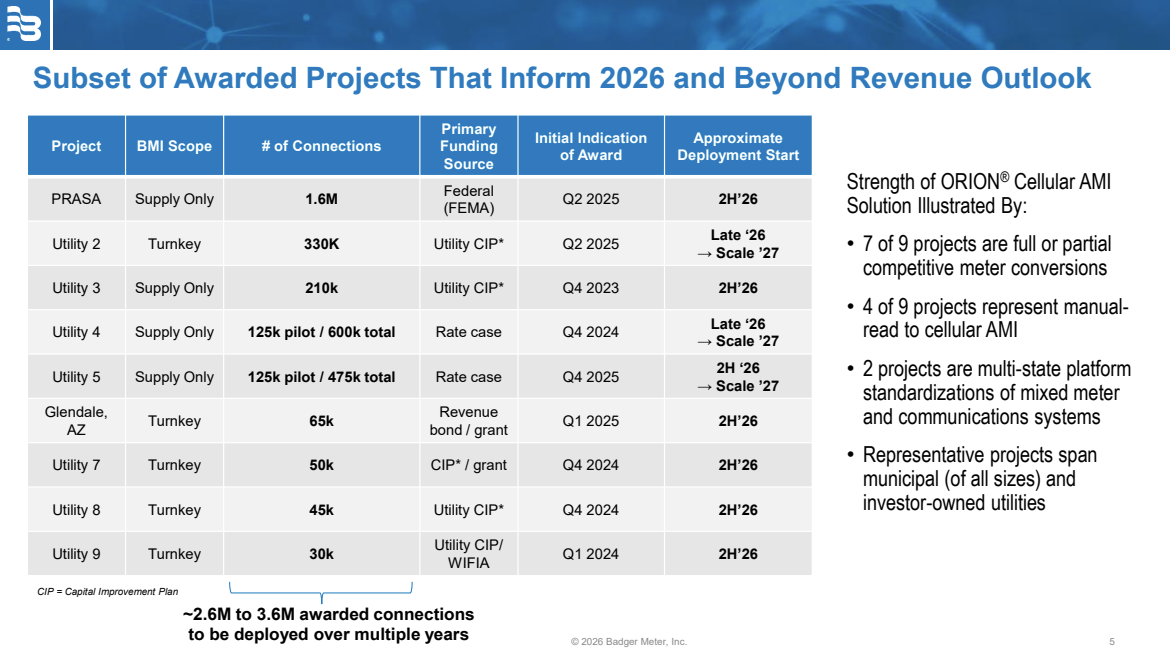

At the same time, the company has already secured several new (and even larger) contracts, including the massive PRASA project in Puerto Rico. The catch is that work on these projects isn’t expected to pick up until the second half of 2026, with some extending into 2027.

Source: Fiscal.AI

As a result, what you end up with is what management calls an “air pocket,” where revenue from old projects slows down before revenue from new projects kicks in. With a business like this, that’s just part of the territory.

Source: Fiscal.AI

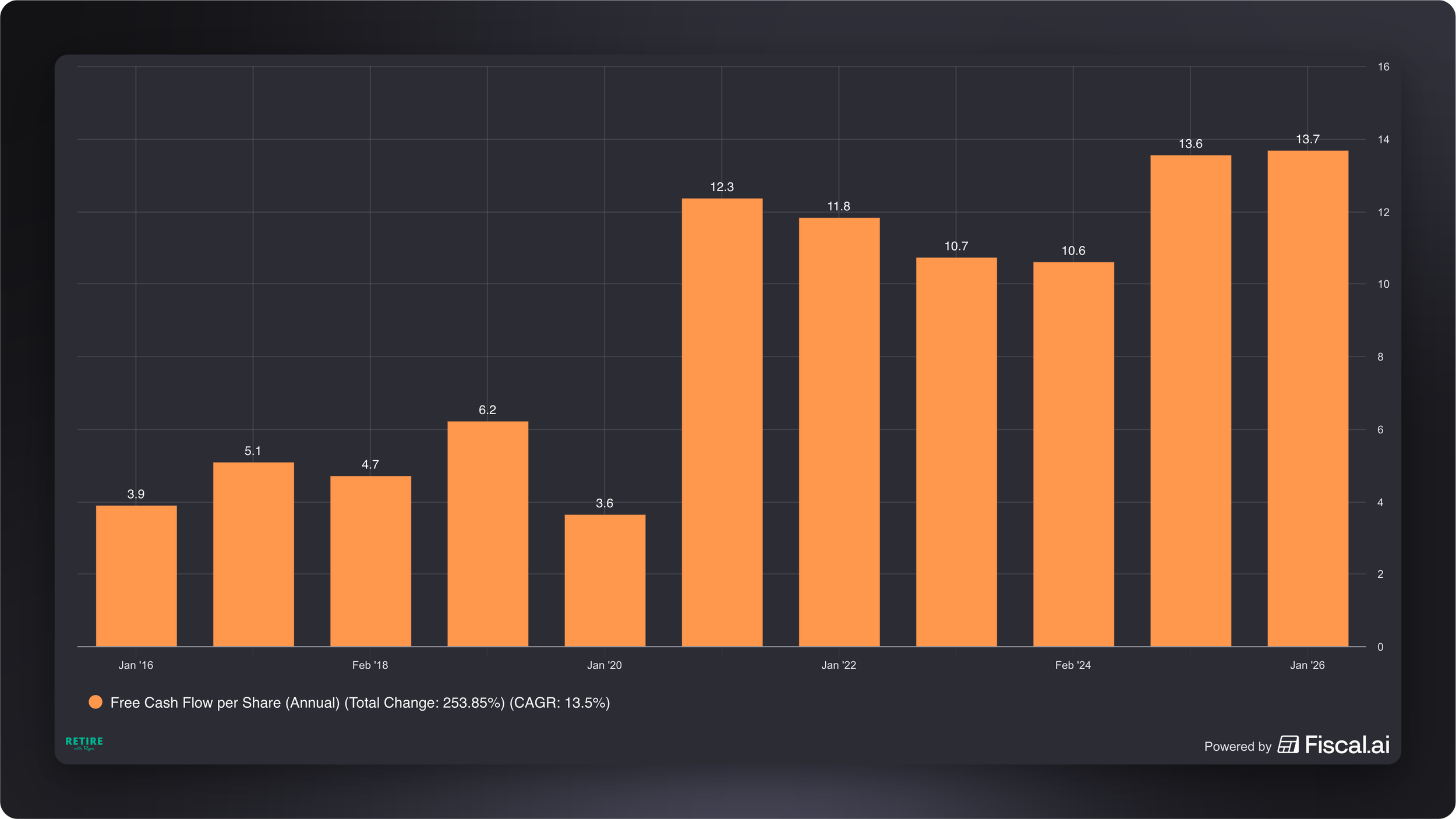

Over time, though, Badger Meter has shown that it can navigate these air pockets pretty well. Growth across the board has been strong, and the company maintains a net-cash position on its balance sheet, which is one of my favorite things to see.

Source: Fiscal.AI

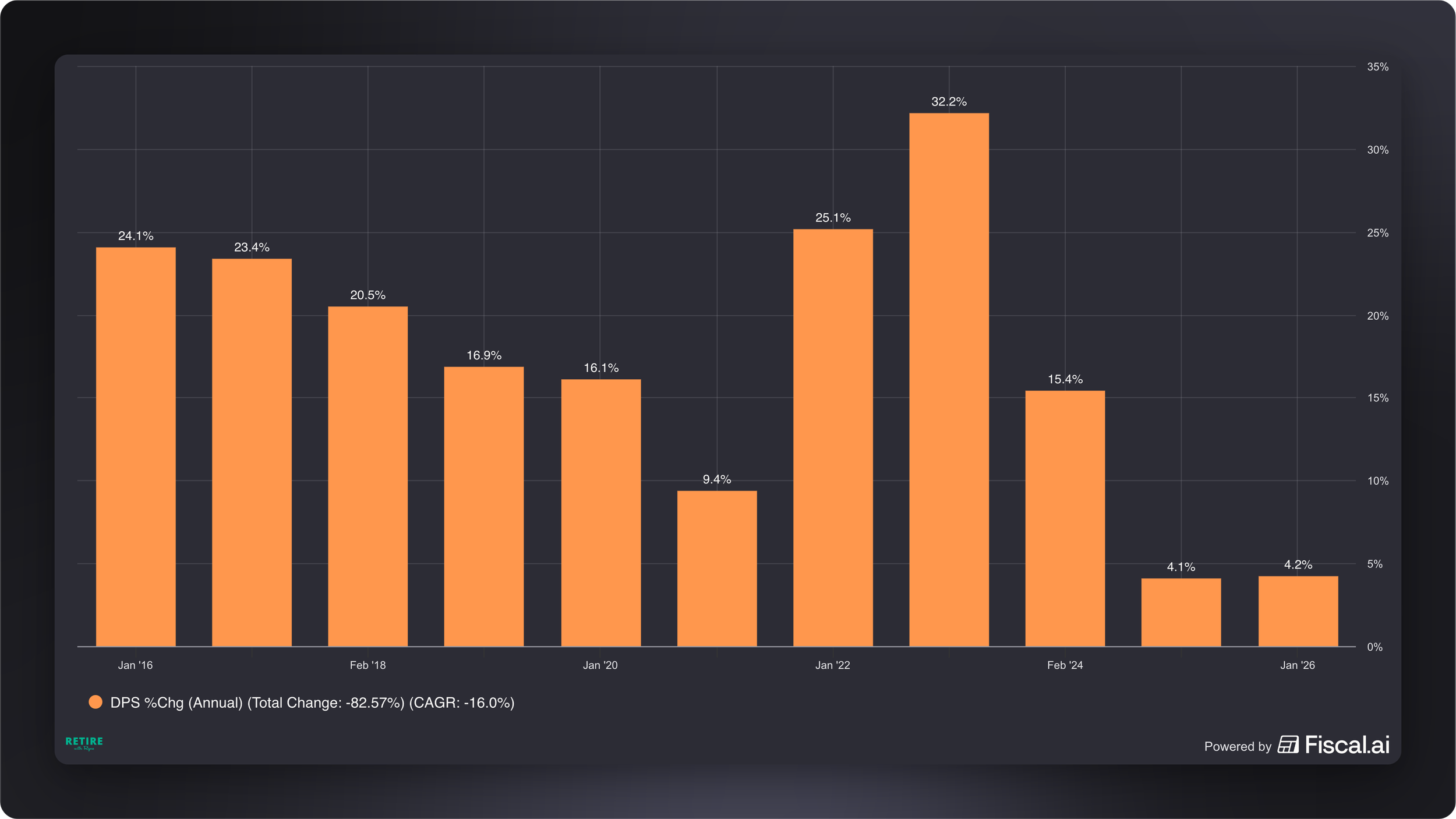

Regarding the dividend, while the starting yield isn’t especially high, it’s actually quite a bit above the company’s historical average, which suggests a potentially good entry point.

More importantly, the dividend growth has been phenomenal. In fact, it’s accelerated in recent years, which makes BMI what I like to call a “dividend rocket.”

All in all, I think this looks like a really interesting opportunity right now. I’m actually considering starting an “exploratory position” in my portfolio (shoutout to Russ for coining the term).

But Badger Meter isn’t the only good buying opportunity out there. There are plenty of other stocks starting to look interesting right now, and I’d love to hear from you: Which discounted stocks do you have your eye on as we make our way into May? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

Blossom is a unique social platform created by investors, for investors. Unlike the usual social media platforms, Blossom is dedicated exclusively to discussions on finance and investing.

I've been actively posting on Blossom for a few years now and I absolutely love the community on there. With over 400,000 DIY investors, Blossom is buzzing with all sorts of different investment ideas. The coolest part is that you can see everyone's full portfolios (including mine), which you can automatically link within the app!

Picture Twitter/X, but with an added portfolio tracking feature and less trolling – that's Blossom for you. Personally, I find it much more enjoyable than my experience on Twitter/X, and I think you will too.

Download Blossom today, and follow me (@ryne) to see my entire portfolio and stay updated on all my real-time investment moves.

IN MY PORTFOLIO 📈

Start tracking your portfolio with Snowball Analytics today—free for 14 days! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

3 DEEPLY Discounted Dividend Stocks To Buy In May 2026

In this video, we'll highlight 3 dividend stocks that have been on the down and out and seem like interesting buying opportunities right now.

CAREFULLY CURATED 🔍

📺 Quality Over Yield - A really great conversation between Jenny Harrington and Jeremy on the Dividend Stockpile channel on what actually makes for a great dividend investment.

🎧 Next Gen Investing - Charles Schwab CEO, Rick Wurster, joins the Master Investor podcast to talk about how one of the largest brokerages in the world is thinking about the future of investing.

📚 Patience Pays Off - Daniel Peris makes the simple, but powerful case for why steady, consistent investing will always beat chasing fast results.

SINCE YOU ASKED 💬

"What are the key indicators that a company’s dividend growth might start slowing down?"

- Vasco | YouTube

This is such a great question. And to answer it, we first have to start with where the dividend actually comes from.

A dividend is paid out of a company’s free cash flow. So after all is said and done—after the company pays for raw materials, employees, marketing, taxes and interest, maintenance, all of it—whatever is left over is free cash flow.

And free cash flow is exactly what it sounds like. It’s cold, hard cash that’s available for the company to use however it wants. They can save it in the bank, pay down debt, make acquisitions, buy back shares, or return it to shareholders in the form of a dividend.

Because of that, free cash flow is really the first thing I’d look at. I’d want to see how it’s growing over time.

If it is, there’s a good chance dividend growth can follow. But if free cash flow starts to slow down, then you can probably expect dividend growth to slow down as well.

A good example of this in action is Lowe’s (LOW), and I say that begrudgingly as a shareholder. Over the past decade, the company’s free cash flow growth has been strong overall, but it’s clearly stalled out over the last couple of years.

Source: Fiscal.AI

And right around that same time, the dividend growth rate started to slow as well—going from consistent double-digit increases to more mid-single-digit raises.

Source: Fiscal.AI

Now, could they have kept raising the dividend more aggressively? Probably. But from a long-term perspective, that wouldn’t be the most responsible thing to do.

If a company continues pushing out large dividend increases without the underlying free cash flow to support it, eventually they hit a wall where they’re paying out more than they’re bringing in. And that’s the opposite of what you want.

So if it were me, I’d focus on two things: how free cash flow is trending, and how that lines up with the payout ratio.

You want to make sure the company isn’t stretching itself too thin just to maintain a high growth rate. To sustainably grow the dividend, having a margin of safety in the payout ratio matters a lot.

Have a question? Ask me here to see it featured in an upcoming newsletter.