Most Investors Think This Is Either/Or...It's Not

Disclaimer: This page contains some affiliate links that might just lead you to the promised land of awesomeness (or at least some cool products). I may receive commissions for purchases made through links in this post.

In the world of investing, it’s commonly agreed that there are two stages of the wealth-building journey: the wealth accumulation stage and the wealth preservation stage.

As you can probably gather, one stage is about building wealth, while the other is about maintaining it. And it’s generally accepted that you’re in the accumulation stage until you reach financial freedom—at which point you transition into the preservation stage.

On the surface, this makes sense. And the neat, either/or labeling checks a box that most investors don’t like to leave unchecked.

We like order, and we like absolutes. So this kind of black-and-white framework fits like a glove. Like most things in investing, though, it’s not that simple.

Even though we like to put things into perfect little boxes, that’s not very practical in the reality we live in. The idea that building wealth and maintaining it are mutually exclusive—and that an investor should neatly fit into one stage or the other—simplifies things, but it isn’t totally correct.

For example, let’s consider someone in retirement. They’re living off their investments and passive income, so we’d naturally say they’re in the preservation stage. And that’s not wrong.

But is an investor in retirement no longer concerned with continuing to build wealth?

We often talk about investing as an infinite game, meaning that it’s something you can play for the rest of your life. There is no end to it.

If that’s true, and if there’s no cap on how large your portfolio can grow, can you not still accumulate more wealth while simultaneously trying to preserve what you have?

In other words, can you not continue to take steps forward while, at the same time, trying not to take steps backward?

Now let’s consider a different investor. This time, think about a young investor with a long time horizon and a long way to go before retirement.

Our natural tendency would be to place this investor firmly in the accumulation stage, and that’s not wrong either. Accumulating wealth is essential if they ever want to reach a point where they can live off their investments.

But does that mean they shouldn’t be concerned with preserving the wealth they’re building along the way?

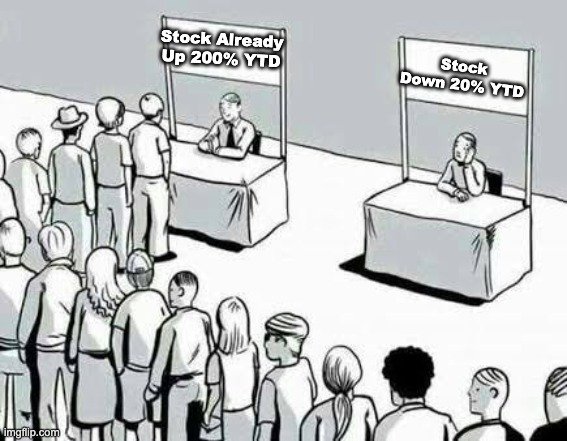

When we talk about movement in the stock market, the conversation almost always focuses on the upside. People like to talk about whose stocks have gone up the most. That’s what’s cool, but it’s very one-directional.

What doesn’t get talked about nearly as much is whose stocks are going down the least during downturns. In other words, nobody pays much attention to who is preserving the most when the market is moving against you.

As we established, accumulating wealth is undeniably essential for the young investor. You need to see your portfolio grow over time.

But that doesn’t mean you should ignore what happens when the market moves in the other direction, which at some point, it will.

I think the problem here is that preservation and accumulation are considered by many to be opposites. In reality, preservation is not antithetical to accumulation—it is a component of it.

If you lose less money during a downturn (more preservation), you don’t need as much upside on the recovery to get back on solid ground (re-accumulation). The two go hand-in-hand.

In my opinion, suggesting that young investors shouldn’t care about preservation is short-sighted. And to suggest that retired investors shouldn’t care about continued accumulation is just as flawed.

In a well-balanced portfolio—or what I like to call an all-weather portfolio—you should aim to have both. You want protection when the market is working against you, and you want the ability to grow when the market winds are at your back.

Having said all of that, now I want to hear from you: How do you personally balance accumulation and preservation in your portfolio? Write to me here and let me know.

Dividend Investing Democratized

Join thousands of savvy investors in the pursuit of early retirement. Get Retire With Ryne delivered straight to your inbox every week as you build your perpetually growing, cash-flowing dividend stock portfolio.

IN MY PORTFOLIO 📈

See my full portfolio with all of my holdings, trades, and dividends on Snowball Analytics! Plus, use code "rynewilliams" at checkout to get 10% off your subscription.

ICYMI 🎥

The Real Reason Most Investors Fail

In this episode of The Deep End, we dive into how AI could reshape investing and whether a future where machines run Wall Street might change the way we think about wealth, work, and retirement.

CAREFULLY CURATED 🔍

📺 Dividend Goals - Dividendology just dropped his latest dividend income update. These videos always get me fired up to invest even more!

🎧 The Pugilist - Terry Smith hopped on Behind the Balance Sheet for a great, no-nonsense discussion on long-term investing and what makes a truly great business.

📚 Outlasting Everyone - Eric Markowitz (author of the upcoming book Outlast) wrote a great piece on the kind of long-term thinking that separates enduring businesses from the rest.

SINCE YOU ASKED 💬

"Where do you see yourself five years from now?"

- @striperkid | YouTube

This is such a great question! And if things go the way I hope they do, I’d love to still be doing exactly what I’m doing right now.

I genuinely love making YouTube videos, writing this newsletter, learning about investing, and sharing those ideas with all of you. Building this little corner of the internet has been an absolute dream, and five years from now, my goal is simply to still be doing this (just hopefully on a bigger scale).

While I’m on the topic, I really do want to say thank you to all of you for supporting the channel and the newsletter. None of this would be possible without people actually showing up to watch, read, and listen to my ramblings each week, so it truly means a lot.

Now from an investing standpoint, I’d also love to see my portfolio much larger than it is today. Ever since it hit $100,000, I’ve really started to notice the compounding effect kick in, which has been incredibly motivating.

Over the next five years, I’d love to grow the portfolio to at least $300,000. If things go really well, maybe we can even hit $400,000.

Outside of that, on a personal level, I’m honestly just very happy with where life is right now. I have a great family, great friends, and a lot to be grateful for.

If the next five years look at all like today, I’d be pretty thrilled with that.

Have a question? Ask me here to see it featured in an upcoming newsletter.

LAST WORD 👋

I love hearing from you all, and I'm always looking for feedback. How am I doing with the newsletter? Is there anything you'd like to see more or less of? Which aspects of the newsletter do you enjoy the most?

Your insights on these matters are essential in making this newsletter the best it can be. If you want to help, take a moment to share your thoughts by completing this quick form. It'll take you less than 60 seconds - guaranteed.

Thanks in advance!